Good morning investors!

Today’s Due Diligence report covers Activision Blizzard.

The video game industry was a benefactor of the pandemic’s stay-at-home mandates and social distancing. Without human interaction, many people turned to consoles, computers, and mobile games for entertainment.

Activision is a major player in the gaming space. And the company experimented with a new revenue model at the perfect time.

But, despite its financial success and franchise acclaim, Activision stock has been a sinking ship — falling 28.7% over the last year.

If this is your first time with us, feel free to subscribe here. If you enjoy today’s newsletter, please hit the heart button at the end of the report.

Now, without further ado...

The Business

Activision Blizzard, Inc. (ATVI) is one of the biggest video game studios in the world. It has its hands in just about every facet of the industry, from full-game development to esports and online community management via its proprietary platform, Battle.net. The company’s key franchises (i.e. big money-makers) include Call of Duty, World of Warcraft, Diabo, Candy Crush, Overwatch, and Hearthstone.

Activision lumps its revenue into two categories: (1) product sales and (2) in-game, subscription, and other. Here’s a description of each category and sub-category.

Product sales: sales of games, both digitally through online marketplaces and physically through retail stores. Through the first three quarters of 2021, product sales accounted for 25% of total sales.

In-game revenue: downloadable content and microtransactions, which represent the sale of virtual currencies and goods that can be used to enhance the gameplay experience.

Subscription revenue: periodic arrangements primarily from the company’s World of Warcraft title, which is an online-only game and generally sold via subscription.

Other revenue: software licensing and licensing of other intellectual property. Collectively, in-game, subscription, and other revenue accounted for 75% of total YTD sales through September 2021.

Activision Blizzard is the product of multiple acquisitions — the biggest being the 2008 merger between Activision Inc. and Blizzard Entertainment (hence the company’s name). Here’s a timeline of other notable acquisitions:

August 1997: Raven Software, an early move that spurred a spree of small studio purchases that would help solidify Activision as an industry leader.

October 2001 & 2003: Treyarch Invention & Infinity Ward, two studios that have played a key role in the development of the Call of Duty franchise — which, as of December 2020, had generated more than $27 billion of revenue since the first series title released in 2003.

February 2016: King Digital, a mobile game developer that Activision purchased to enter a new market.

Activision’s acquisition strategy over the last 20 years has paid off handsomely. Beyond bolstering the development teams behind franchises like Call of Duty (which also helped expedite game rollouts, although that can create problems too), adding development teams to the corporate umbrella paved Activision’s way into the lucrative mobile games market.

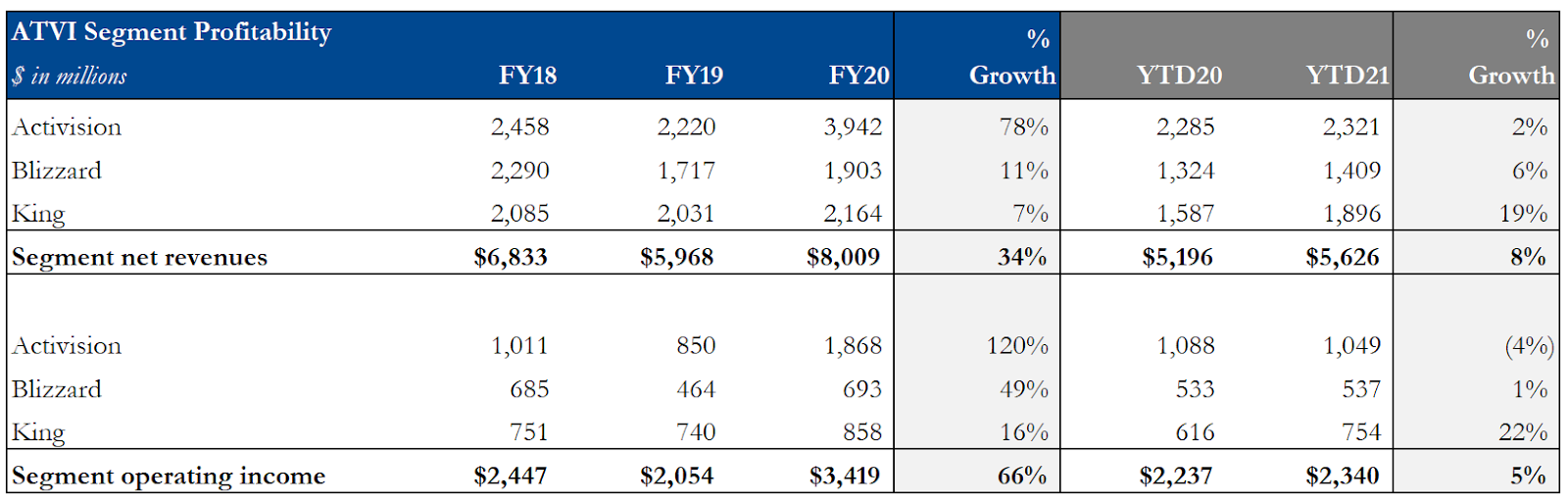

The company operates through three segments: Activision, Blizzard, and King. Their financial contributions are outlined below. Note: the table does not account for non-reportable segments, the net effect of deferred revenue, and intersegment revenue.

The Activision segment ballooned in FY20 as the company unveiled its rendition of battle royale, Call of Duty: Warzone in March 2020. This game style, which has taken off in recent years, usually leverages a free-to-play (F2P) revenue model.

Video game developers have rapidly incorporated the F2P into their commercialization strategies. Unlike the traditional pay-to-play model (P2P), in which players pay a one-time fixed price upfront, this model grants players free access to a particular game and typically features purchasable in-game content. And, from a revenue perspective, it works well. One study has shown that F2P mobile game players spent an average of $87 while console players spent $92. For comparison, premium P2P console games typically start around $60.

The Narrative

Activision has been a news headline staple for all the wrong reasons lately. While there are plenty of storylines to dissect, like the delays of Diablo and Overwatch 2 or China’s crackdown on video games, the major plot point in Activision’s narrative relates to cultural issues that could cause the company to implode if left unfixed.

Strikes, Allegations, Investigations, and Lawsuits galore

“I want Activision Blizzard to be the leader in our industry for workplace culture.” –CEO Bobby Kotick on the company’s Q3 earnings call.

It’s all fun and games until…well…it’s not. You might be surprised to hear that the video game industry is notorious for extreme working conditions and abysmal pay structures — such as unpaid overtime — especially among lower-end employees like quality assurance testers. Activision is no exception. In December, roughly 200 Activision employees reached a breaking point after several QA employees were let go, inciting a labor strike and efforts to unionize.

Unfortunately, this isn’t the most damning piece of news for Activision in the last few months.

About a month before the labor strike, the Wall Street Journal published a monumental report, titled: Activision CEO Bobby Kotick Knew for Years About Sexual-Misconduct Allegations at Videogame Giant.

The in-depth story outlines the company’s lengthy history of quietly dismissing internal complaints by female employees, which alleged discrimination and harassment. Last summer, the California Department of Fair Employment and Housing filed a lawsuit against Activision. The company is described as having a “frat boy” culture in which excessive drinking and employee misconduct is encouraged. And there’s plenty of evidence that indicates Kotick knew about these issues and actively suppressed them. Per the report:

[Internal documents] show that he knew about allegations of employee misconduct in many parts of the company. He didn’t inform the board of directors about everything he knew, the interviews and documents show, even after regulators began investigating the incidents in 2018. Some departing employees who were accused of misconduct were praised on the way out, while their co-workers were asked to remain silent about the matters.

As more information has come to light, more signs point to Kotick’s eventual departure. Over the last few months, ATVI’s share price has slumped. Key partners, like Xbox and Sony, are second-guessing their relationship with Activision. A petition for the removal of Kotick has reached almost 1,900 employee signatures. Even Wall Street analysts are calling for Kotick to depart the company. The belief is that only then can Activision right its course and move forward.

Supposedly, Kotick has told colleagues that he would step down if he can’t quickly fix these piling issues. But it remains to be seen if that’ll happen anytime soon.

Stock Overview

ATVI compares favorably to its peers from an earnings metric standpoint. For instance, Take-Two Interactive (TTWO) and Electronic Arts (EA) — two video game competitors — have P/E ratios of 32.38 and 48.86, respectively. That’s well above ATVI’s ratio of 19.17.

The same can be said for their price-to-book ratios of 5.19 and 4.72, relative to ATVI’s 2.98. Note: P/B compares a company’s market value to its book value — the net assets of a company (i.e. if a company liquidated its assets and paid off all of its debt, the remainder would be book value).

The Finances

Revenue Highlights:

Video game producers are subject to cyclicality thanks to the timing and reception of yearly product slates. 2019 was a prime example. Activision bounced back with a strong 2020, backed by the release of Call of Duty: Warzone, a free-to-play modeled game that’s been quite successful.

Activision’s mobile game sales are much steadier than its games for consoles and PCs, which helps insulate the company from some of that seasonal volatility.

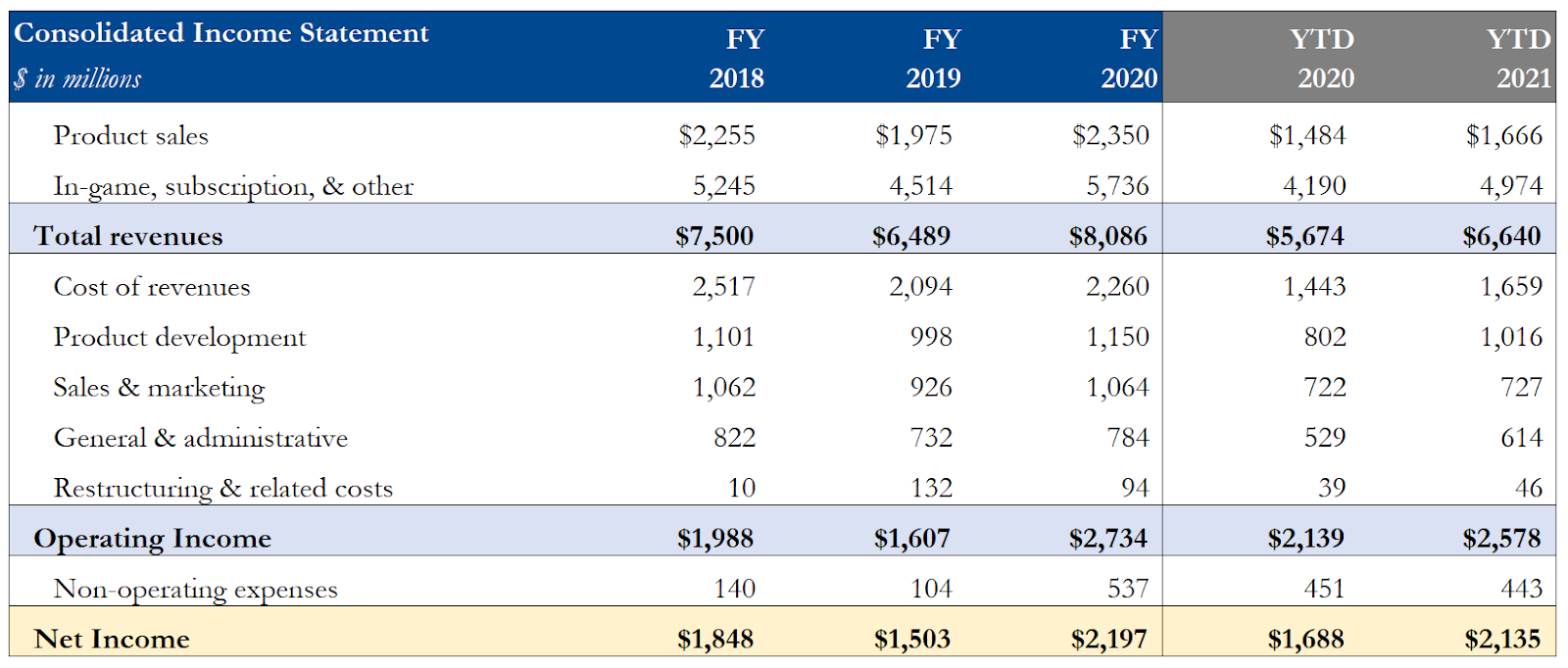

Through September of 2021, Activision has increased total revenue by 17% year over year — driven by growth and strategy execution across each of its business segments. The King business segment was responsible for much of that growth as revenue rose almost 20% relative to YTD 2020 and Candy Crush was once again the top grossing game franchise in US app stores.

Profit Highlights:

Management noted on its latest earnings call that it added hundreds of developers to its team in the third quarter, which led to an increase in product development costs.

Although Activision’s business model is susceptible to some revenue fluctuation, its margins are consistently healthy. From FY19 to FY20, the company’s operating income margin increased from about 24.8% to 33.8% as a result of increased in-game purchases (again, another benefit of the free-to-play model). The same goes for the first three quarters of 2021, which saw OI margin jump even higher to 38.8%. Couple that with limited interest expenses, and you can see why Activision has pumped out steady profits.

Through the first three quarters of 2021, ATVI had already grown it’s net income by 27% relative to the same period in 2020 — a positive sign ahead of the fourth quarter, which is typically a massive quarter thanks to holiday season releases.

Balance Sheet & Cash Flow Highlights:

Activision’s balance sheet is in good shape, with cash and debt balances of $9.7 billion and $3.6 billion, respectively. In other words, the company has sufficient liquidity to pay off its debt in full, if it needed to, with plenty left over to fund operations and other initiatives.

Activision generated $2.8 billion of free cash flow on a trailing 12-month basis — a 45% year-over-year increase — aided by not having a significant need for capital expenditures.

Earnings Trends

ATVI has a lengthy history of meeting or surpassing its earning guidance, only missing two consensus estimates in the last five years.

The Primary Strengths

Industry growth. The gaming industry was a winner of the pandemic’s radical new “normal.” So much so that a report estimates that the global games market generated $177.8 billion of revenue in 2020, a 23.1% increase relative to 2019. And the demand for video games hasn’t declined in 2021, at least not in the US. Per The NPD Group’s Q3 Games Market report, overall total consumer spending on video gaming in the US totaled $13.3 billion in the third quarter of 2021 — a 7% year-over-year increase. Considering Activision is one of the largest video game companies, it’s well-positioned to benefit from this broader economic trend.

Strong franchises. Activision’s product lineup features some of the world’s most well-known and successful franchises in the world, including Call of Duty, World of Warcraft, Overwatch, and Candy Crush. Just as movie sequels can fall short of expectations, success isn’t guaranteed in the video game industry. But it’s safe to say these franchises have massive, global followings. That doesn’t hurt.

Financial health. Cultural issues aside, the company is in a healthy financial position. Of course, that’s not guaranteed to last if the alleged toxic workplace continues to deter talent and eventually chase away key business partnerships. But as of September 2021, cash balances dwarf debt and the company routinely has healthy income margins.

The Primary Risks

Business disruption. At this point, Activision is embroiled in controversy. Employees are on strike. The SEC is investigating allegations of misconduct. Corporate partners are rethinking their relationship with Activision. People are calling for Kotick to stand down. That’s all very bad for business — and has the potential to get worse before it gets better.

Talent acquisition and retention. Human capital is a necessity in the gaming industry. If Activision’s cultural issues continue, they’ll have a hard time onboarding and keeping the industry’s best game developers, testers, publishers, and distributors. That would translate to lower quality products and lost customers. Unsurprisingly, this is a pressing issue for Activision. Per the company’s latest 10-Q:

We have experienced challenges in both the retention of our existing talent and attraction of new talent, with our average voluntary turnover rates being higher in the current year as compared to the prior year in many parts of our company. This competition, voluntary turnover and recruiting difficulty, has negatively impacted our ability to deliver future game releases, and if they persist, could continue to negatively impact our ability to deliver content in a cadence that will be optimal for our business.

Franchise concentration. The titles mentioned above comprise over 70% of the company’s revenue. Considering the competitiveness and cyclicality of the video game industry, Activision is subject to revenue swings in the event of underperformance — or product delays— from one or more of these franchises. During the company’s Q3 earnings call, management shared that the upcoming Fall 2022 releases for the Overwatch and Diablo franchises may not hit shelves until 2023.

The Street’s Opinion

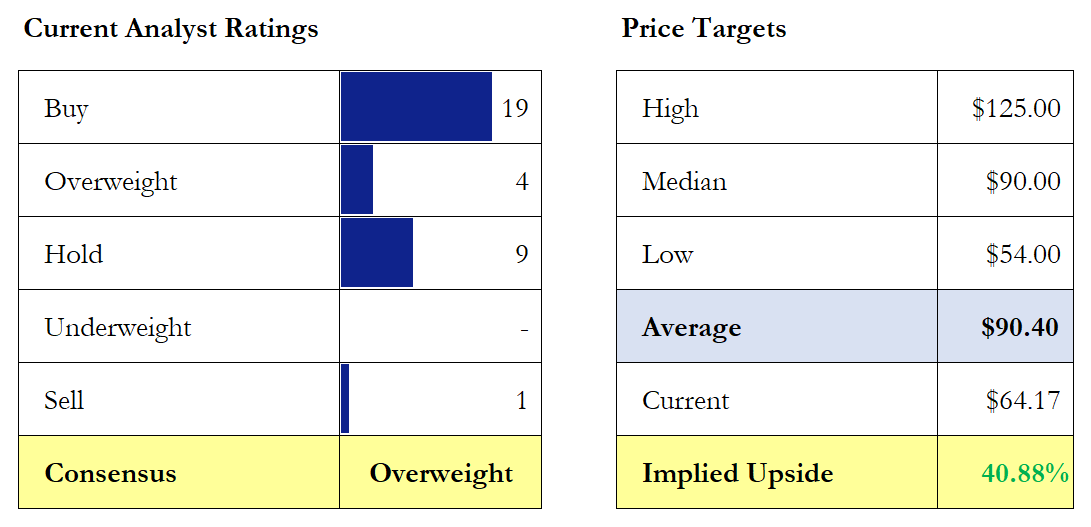

Despite its cultural issues, ATVI registers an “Overweight” consensus rating. The stock’s average price target of $90.40 implies an upside of 40.9%, while the lowest price target implies things could get worse before they get better. Should Kotick step down, Activision’s public perception (and share price) could improve drastically.

Bullish or Bearish?

From a morality standpoint, it’s easy to make a case against Activision — especially while Bobby Kotick is at the helm. No one wants to be associated with someone who condones such a toxic workplace, whether that’s consumers, talent, or strategic partners. Eventually, such a perception will trickle down to Activision’s plump bottom line.

That said, from a purely financial and operational standpoint, Activision is in much better shape than its corporate culture.

Activision’s IP is established and highly acclaimed. So long as developers stay to oversee them, franchises can continue to churn out desirable and lucrative titles.

Each reporting segment generates operating income at healthy margins, thanks to strategic execution related to increased in-game purchases across the board.

Free cash flow is ample, giving the company plenty of capital to fund future projects and potential acquisitions.

With these strengths in mind, I’m conditionally bullish on Activision, which currently trades not too far above its 2020 low. The condition being that Kotick is not in place much longer — or the world somehow forgives or forgets the company’s internal transgressions.