Are CLOs a threat to the financial system?

A look at collateralized loan obligations and their risks.

Good morning, investors!

If this is your first time with us, don’t forget to subscribe here. If you enjoy today’s issue, please hit the heart button at the end of the report.

Without further ado…

Are CLOs a Looming Problem?

Ah, controversy — where would the financial world be without it? Indeed, Collateralized Loan Obligations (CLOs) have stirred up their fair share of debates over the years, often playing the role of the misunderstood anti-hero in the financial narrative.

Back up, what are CLOs?

A CLO is a financial instrument that bundles corporate loans into different risk levels called "tranches" (essentially, slices of the pie). The loans within a CLO are typically high-yield, high-risk loans (also known as "leveraged loans") made to businesses with less-than-stellar credit ratings. Since each tranche of the CLO has a different risk level, it also offers different interest rates for investors. The lower the risk, the lower the return; the higher the risk, the juicier the potential payoff.

Here’s a good visual of a CLO’s structure from Oaktree Capital; notice that losses from any defaulted loans are absorbed from bottom (equity, the riskiest tranche) to top (AAA, the safest).

The main reason CLOs are controversial lies in their close resemblance to the notorious Collateralized Debt Obligations (CDOs), those financial Frankensteins that were instrumental in the 2008 financial crisis. Because CLOs and CDOs are both structured products involving the pooling and tranching of various assets, some investors can't help but raise an eyebrow at the possibility of history repeating itself. That’s particularly true when recessionary fears disseminate throughout the masses, which was the case during 2020’s pandemic-induced bear market.

What CLO critics and proponents have to say

Critics argue that CLOs can obscure the underlying loans, making it difficult for investors to assess the true level of risk. The concern is that this could result in a domino effect of defaults, reminiscent of the subprime mortgage crisis. Additionally, because CLOs often consist of high-risk, leveraged loans, they may contribute to excessive risk-taking and speculation in the financial markets. In plainer terms, greed has a history of blowing up in our faces.

“The Looming Bank Collapse,” by Frank Partnoy, was published in The Atlantic in the summer of 2020. As you can probably guess, the catalyst of Partnoy’s “looming collapse” prediction was/is the CLO.

“Despite their obvious resemblance to the villain of the last crash, CLOs have been praised by Federal Reserve Chair Jerome Powell and Treasury Secretary Steven Mnuchin for moving the risk of leveraged loans outside the banking system. Like former Fed Chair Alan Greenspan, who downplayed the risks posed by subprime mortgages, Powell and Mnuchin have downplayed any trouble CLOs could pose for banks, arguing that the risk is contained within the CLOs themselves.

These sanguine views are hard to square with reality. The Bank for International Settlements estimates that, across the globe, banks held at least $250 billion worth of CLOs at the end of 2018. Last July [2019], one month after Powell declared in a press conference that “the risk isn’t in the banks,” two economists from the Federal Reserve reported that U.S. depository institutions and their holding companies owned more than $110 billion worth of CLOs issued out of the Cayman Islands alone. A more complete picture is hard to come by, in part because banks have been inconsistent about reporting their CLO holdings. The Financial Stability Board, which monitors the global financial system, warned in December that 14 percent of CLOs—more than $100 billion worth—are unaccounted for.”

TLDR: Contrary to key government officials’ opinions (shoutout Jerome), CLOs still pose a significant threat to the financial system because banks are, in fact, invested in them.

On the other hand, proponents of CLOs maintain that they are fundamentally different from the villainous CDOs. They argue that the loans in CLOs are diversified across industries and borrowers, reducing concentration and correlation risks. Furthermore, CLO managers actively manage the loan portfolios, unlike the static pool of assets in CDOs.

Around the same time as Partnoy’s article, Wharton finance professors Michael Roberts and Michael Schwert shared an opinion piece that took the opposite side of the argument. The UPenn tandem pointed to the performances of these two investment vehicles during the 2008 crisis as a prime example of their fundamental differences:

“A study by Cordell, Feldberg, and Sass (2019) shows that AAA-rated tranches of CDOs issued before the 2008 crisis lost $325 billion during the following years. In contrast, Standard and Poor’s found that AAA-rated tranches of CLOs issued before the 2008 crisis lost nothing. This performance differential stems from differences in the assets that the two vehicles bought.

The CDOs that got into trouble during the financial crisis did not buy loans, they bought junior tranches of other CDOs (mortgage-backed securities) and credit default swaps (derivatives) referencing other CDOs. The process of repackaging CDO tranches into new CDOs significantly amplifies risk, which is why senior investors in those products lost so much money.

The typical CLO holds hundreds of loans diversified across dozens of industries. Exposure to any industry is contractually limited to 15% of the loan pool, while the maximum exposure to a single company is 2%. Thus, defaults must be pervasive across all sectors of the economy to materially affect the collateral pools of CLOs.”

TLDR: During the ‘08 financial crisis, the CDO market collapsed while CLOs were fine. This would suggest that CLOs are more structurally sound than CDOs, which, during the crisis, often magnified their risk by doubling down on other CDOs.

How exposed are US banks to CLOs?

In the event of CLO chaos, the biggest concern would be the impact on banks, which represent the heart of the financial system. That wasn’t lost on the Wharton professors, who shared the CLO holdings of three major banks at the time:

“U.S. banks hold $104 billion of CLO investments, $83 billion of which sits on the balance sheets of three banks: JPMorgan Chase, Wells Fargo, and Citigroup. As a fraction of their assets, CLO investments are 1.1%, 1.3%, and 0.9%, respectively. As a fraction of Tier 1 capital, which regulators use to measure a bank’s ability to withstand losses, CLO investments are 17%, 17%, and 14%, respectively.”

In other words, CLOs represented a small percentage of their asset base. That was 2020 though, what about today?

As of December, collectively, JPMorgan, Wells Fargo, and Citigroup have about the same amount invested in CLOs ($103.5 billion) as the US banks held at the time of Roberts’ and Schwert’s article ($104 billion). So, a net increase of roughly $20 billion, although JPM and WF are responsible for 98% of that total figure. Citigroup’s wasn’t as detailed in their public filings, but their total exposure to CLOs was much smaller at $2.6 billion.

So, JPM’s and WF’s shareholders' equity and retained earnings (i.e., tier 1 capital) are about four times the size of their CLO exposure. Less cushion than three years ago, but still an ample level of cushion.

What would it take for a doomsday scenario to occur?

To ask that another way, what would it take for CLOs to initiate the same level of widespread damage as CDOs did in 2008? According to Roberts and Schwert, unprecedented defaults, but we’d have bigger problems anyway.

“If lenders were to recover $0.40 on the dollar for loans in default, then 60% of the loans in CLO portfolios would have to default before the AAA-rated tranches would even begin to lose money. To put that number in context, the cumulative default rate for risky debt during the worst three years of the Great Depression (1931-1933) was 31%.

If AAA-rated CLO investments default in large numbers, then the business sector will be facing its worst downturn in the history of our country. CLOs will be the least of our concerns.”

Are CLOs a problem right now?

Naturally, rising interest rates aren’t ideal for leveraged loans and, thus, CLOs. It’s common for businesses to roll existing loans into new ones as they mature (a process known as refinancing). Except when interest rates are high, there’s less appetite for risk from lenders, meaning access to capital recedes and many businesses can’t pay their debts. Surprise, surprise — expect leverage loan default rates to rise.

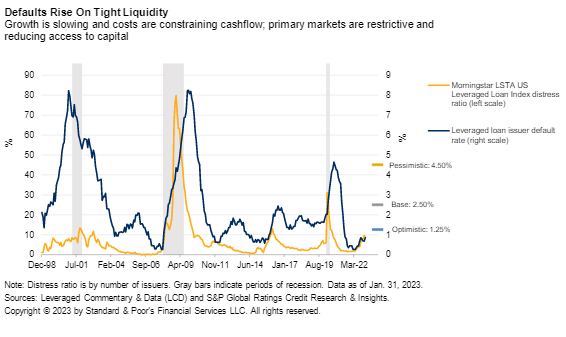

Standard & Poor’s projects default rates to rise from 0.8% in January to anywhere between 1.25% and 4.5% by December, depending on whether you’re a glass-half-full or glass-half-empty kind of forecaster.

In a broader context, here’s a historical charting of leveraged loan default rates (blue line) and Morningstar’s leveraged loan distress ratio (yellow line) — which is the ratio of leveraged businesses entering/in default relative to the total number of leveraged businesses. In other words, defaults likely rise by the end of 2023, but not to the levels of the dot-com bubble or financial crisis.

Long story short, CLOs may not be our economy’s next undoing, but they’re certainly still something to keep an eye on.

Thanks for reading. Don’t forget to hit the heart button if you enjoyed today’s report.

If you haven’t subscribed already, you can do so here.