Lithium spot prices are slipping. Are lithium miners in trouble?

A Chinese battery maker sent shockwaves through the industry.

Good morning, investors!

If this is your first time with us, don’t forget to subscribe here. If you enjoy today’s issue, please hit the heart button at the end of the report.

Without further ado…

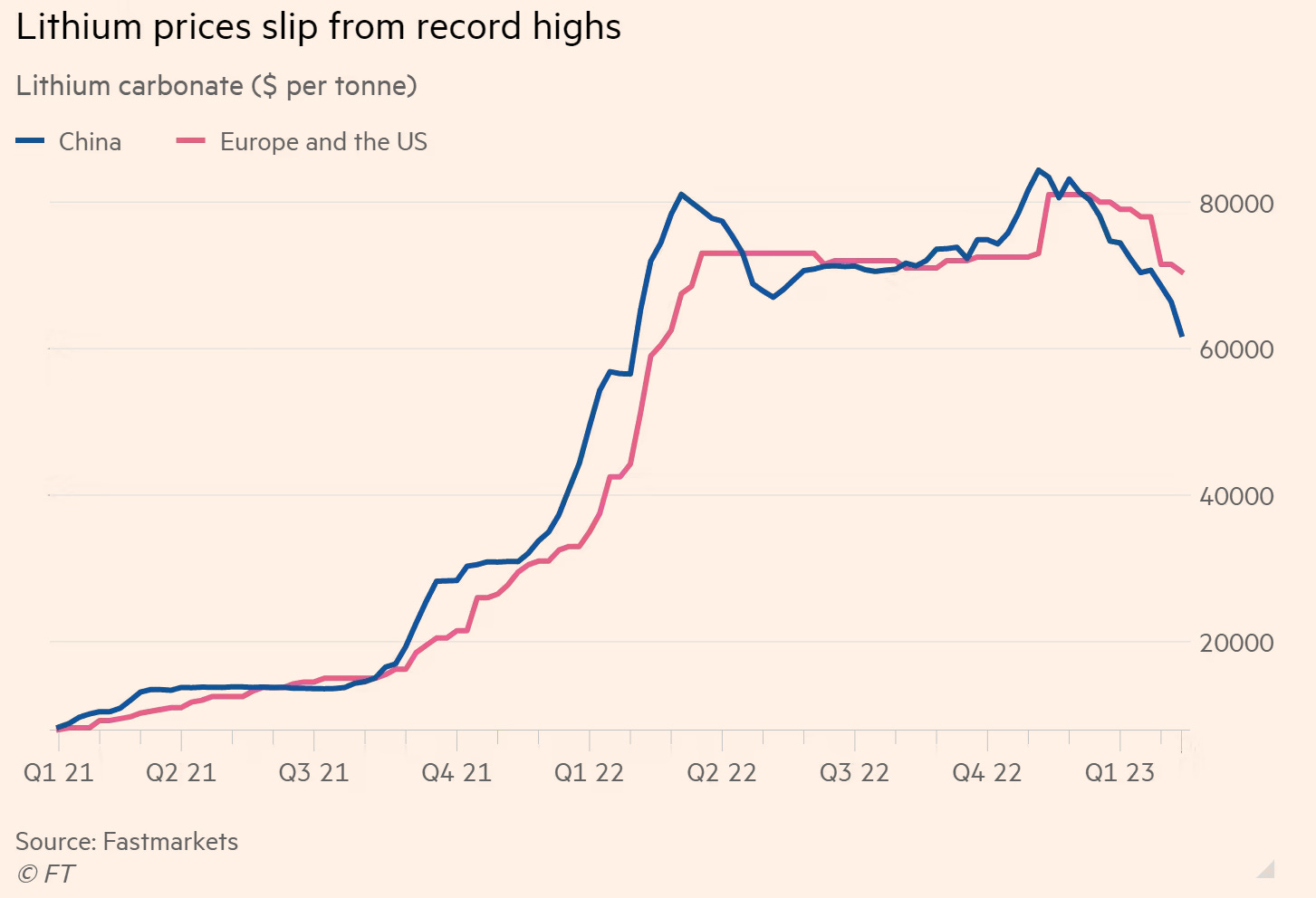

It’s well-documented that lithium demand is expected to outpace supply in the coming years, so owning and operating lithium mines could be a very lucrative venture — high lithium prices translate to high revenue.

But prices have slipped a bit in recent months.

And they could slip even more.

On Friday, February 17, lithium stock prices suddenly tumbled down the mineshaft, as the likes of Albemarle (ALB), Livent (LTHM), SQM (SQM), Piedmont Lithium (PLL), and Lithium Americas (LAC) lost about $6.6 billion in market value, collectively.

But why?

CATL Adjusts Its Pricing Strategy

If you’re familiar with the EV industry, you should know the name Contemporary Amperex Technology — or CATL. The Chinese battery maker accounted for almost 40% of global EV battery sales in 2022, making CATL the world’s top producer.

In 2022, CATL tethered its battery prices to lithium, which means the spike in lithium prices was passed onto the battery maker’s customers. Suffice to say, as the world’s biggest producer, CATL has some pricing power when it comes to lithium-ion batteries.

So, it’s no wonder that lithium stock prices dropped when CATL announced a major adjustment to its pricing strategy for strategic partners, such as NIO, Li Auto, Huawei, and Zeekr. In exchange for buying 80% of their EV batteries from CATL, these Chinese automakers could buy batteries at a bit under $30,000 per ton of lithium carbonate. (Current prices are about $55,000.)

Why cut prices?

If you’re an automaker that’s investing heavily in EV rollouts, five-figure price tags are scary — they eat into margins. In turn, more and more automakers are following in Tesla’s footsteps and becoming battery makers too, such as Ford, GM, Toyota, and Honda.

Nio is a recent addition to this list — the Chinese automaker plans to open a battery plant that’s expected to power about 400,000 EVs per year.

By giving some of its biggest customers the option to secure cheaper batteries, CATL can continue to scale its battery operations.

Why cut prices so drastically?

It can afford to. CATL mines some of its own lithium, so it’s willing to sacrifice mining profits to sell more batteries and remain in the pole position.

What does this mean for lithium miners?

That remains to be seen. On one hand, falling lithium prices should hurt mining margins. On the other hand, demand should continue working in favor of lithium prices and sales. At least one major lithium player expects China to remain in growth mode; here’s Kent Master, President, Chairman, and Chief Executive Officer of Albemarle.

We continue to expect EV sales in China to grow 40% year over year, an increase of nearly 3 million vehicles.

Our contract customers are not slowing down their ordering patterns, and early indications are both that cathode inventory and battery inventory in China are decreasing, which is a good sign for lithium sales.

Three Eye-Opening Tweets

And finally, we close with three eye-opening tweets.

The new Mexico is…New Mexico (in terms of oil production).

Was this real…?

A thread on Buffet and BRK.A’s performance over the years :

Thanks for reading. Don’t forget to hit the heart button if you enjoyed today’s report.

If you haven’t subscribed already, you can do so here.