Good morning, investors!

We’re putting a different spin on today’s edition of Market Movers. Rather than shed light on a stock that’s made a splash in the market recently, we’re going to highlight a stock that could experience some tailwinds based on undervalued fundamentals.

Today’s company is National Mortgage Insurance Corporation.

If this is your first time with us, feel free to subscribe here. If you enjoy today’s newsletter, please hit the heart button at the end of the report.

Now, without further ado...

National Mortgage Insurance Corporation is — you guessed it — a mortgage insurance company, which trades under its holding company, NMI Holdings (NMIH). When wannabe homeowners take out a conventional mortgage but bypass a 20% down payment, they’re required to get private mortgage insurance (PMI). In turn, the lender is protected against losses if the homeowners can’t pay the loan because the insurer foots the bill.

Generally, mortgage borrowers can cancel their PMI once their loan-to-value ratio dips under 78%. Until then, the insurers collect monthly premiums. This is how NMI makes money.

Considering the surge of home purchases this year — partially thanks to my generation’s collective decision to buy homes so that their canine children can have yards — you would think the mortgage insurance industry would be raking in insurance premiums.

And you would be right. Here are NMI’s premium earnings by quarter since the end of 2018.

Since 4Q18, NMI’s net premium earnings have increased by 60%. Business is booming.

Yet, shares of NMIH are down nearly 38% over the last year and a half.

What happened?

You don’t need dates to make an educated guess: the pandemic.

For starters, we entered a temporary bear market that depressed companies across all industries. More specifically to NMI, forbearance programs rolled out throughout the country, enabling financially distressed borrowers to pause their mortgage payments, including PMI premiums. (Here’s a good overview of forbearance.)

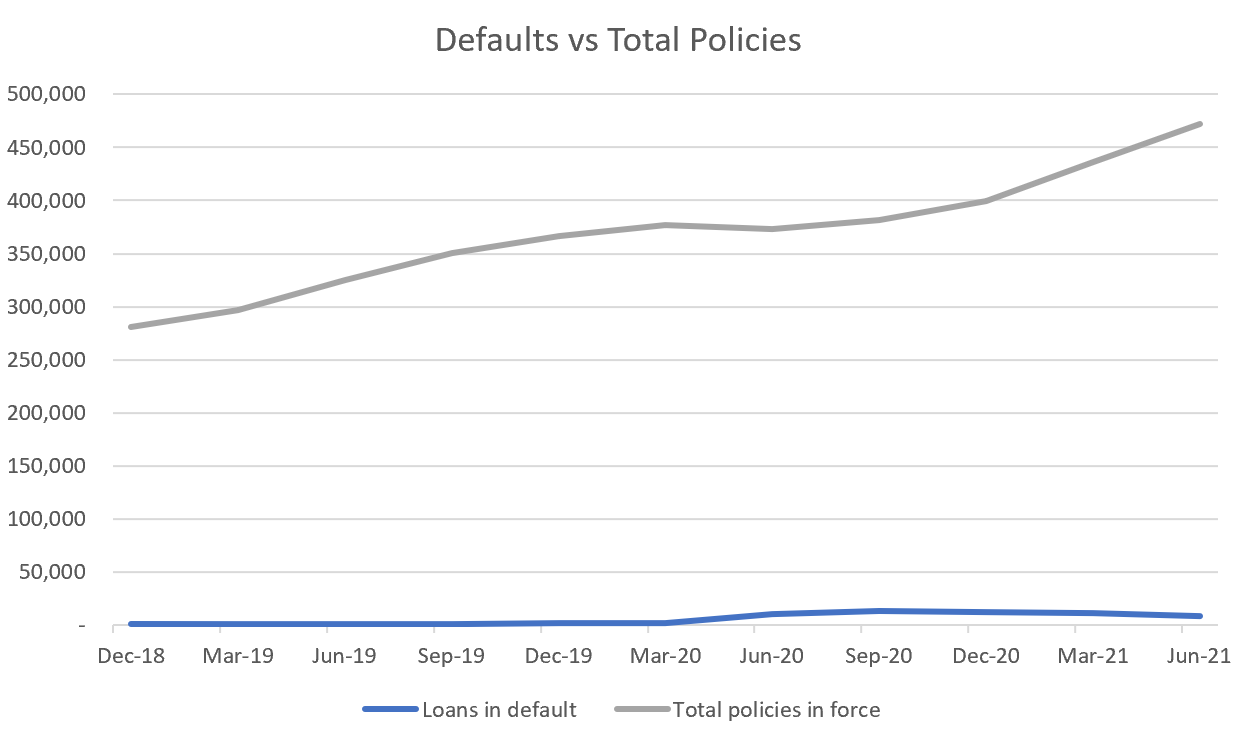

Consequently, as borrowers entered forbearance, NMI experienced a sizable increase of (a) loans in default and (b) risk in force on defaulted loans (the amount NMI could potentially be on the hook for). Loans in default — which don’t represent claims — peaked at 13,765 a year ago; this represented risk in force of $1.01 billion.

As of June 30, those numbers have dipped to 8,764 and $625 million, respectively. Of those loans in default, roughly 90% were enrolled in a COVID-related forbearance program. So, these borrowers are treated as in default since they aren’t paying, but lenders have granted them leeway while they’re in forbearance.

While these numbers may seem high, it’s important to step back and look at NMI’s portfolio from a broader perspective. NMI’s in-default loans comprise only 1.86% of its total policies in force.

One of the reasons NMI’s default rate has remained so low is the creditworthiness of its borrowers. Borrowers with credit scores above 700 represent roughly 97% of NMI’s portfolio; only 8.8% of borrowers had loan-to-value ratios above 95%.

Financial Highlights

Although loans in default remained low relative to NMI’s total policy count, insurance claims still popped to $59.2 million in FY20 — a 374% year-over-year increase.

NMI’s total revenue growth helped insulate it from these insurance payouts though. In FY20, net income experienced a negligible decline of $400 thousand despite the pandemic’s fallout.

Through the first six months of 2021, insurance claims and claim expenses are down significantly relative to the same period in 2020; net premiums earned are up 9.7%.

Although earnings didn’t experience much of an impact, the company issued 15.9 million shares in June 2020, which helped the company raise almost $220 million. While this capital injected NMI with capital during a period of uncertainty, it also suppressed EPS.

That said, the housing market boom has helped EPS figures recover.

Potential Hurdles

What happens when forbearances end? The financial consequences of the pandemic (e.g. furloughs, layoffs, pay cuts, less work in general) made it difficult for many people to pay their debt. To ease this burden (and prevent widespread foreclosures) forbearances programs’ enrollment skyrocketed. But the debt doesn’t go away. As those programs conclude and borrowers are required to make loan payments again, there’s likely to be an uptick in loan defaults and, thus, an uptick in claims. That works against NMIH’s bottom line.

Here’s what Brad Shuster, NMI’s Executive Chairman, had to say about the issue during the company’s last earnings call.

The forbearance programs have been enormously valuable helping borrowers bridge from a point of acute stress to a much more stable position today. And the expanded set of modification and payment deferral options introduced early in the pandemic have helped a borrower successfully transition out of forbearance and default status. But as the programs wind down there will undoubtedly be some who are still struggling and forbearance will work for most, but not necessarily for all. And for this group, we expect there'll be another policy response because it doesn't make sense to leave these borrowers in forbearance on a perpetual basis, but it also isn't fair, and it doesn't make sense to cut them loose without support at the end of the foreclosure process.

Adam Pollitzer, the company’s CFO, added:

And just to layer on to that, our broad view is that there will be additional support that's offered. It certainly aligns with all of the conversations that have happened thus far in DC, even what we're seeing over the last few days in focus around an eviction moratorium, which is a rental focus, but it shows the eagerness to provide support.

In short, NMI management believes the government will continue assisting borrowers in need. Despite this belief, the company has still modeled its reserves off of the assumption that forbearance programs aren’t extended — a conservative and prudent approach. As of June, NMI’s reserve for insurance claims and claim expenses was $101.2 million; in addition, NMI had a portfolio of available-for-sale bonds valued at $1.99 billion.

What happens when interest rates rise and the market cools? As America re-opens its doors and the economy awakens from a pandemic slumber, the Fed must now consider whether it’s time to raise rates — which would eventually trickle to the mortgage industry. During their June meeting, Fed officials were somewhat split on when they think they’ll raise interest rates from near zero. Seven expected to increase rates in 2022; 13 out of 18 members expected to raise rates by 2023.

Rising mortgage rates would discourage people from buying homes, meaning fewer mortgages and insurance premiums. However, NMIH’s fixed income investments would benefit from rising rates, partially offsetting the downside of an industry-wide dip.

The Street’s Opinion

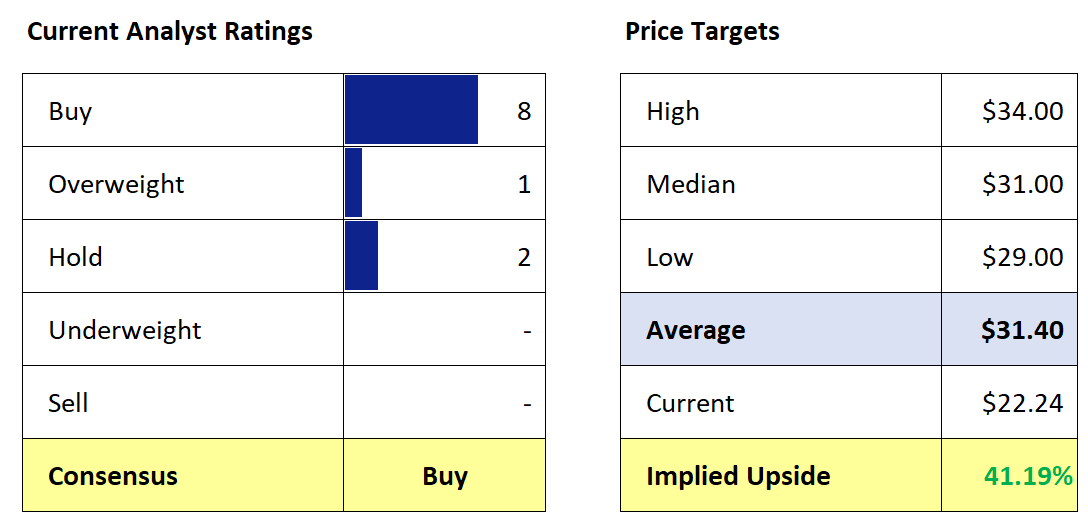

NMIH has quite a few analysts in its corner. Thanks to eight buy ratings, one overweight, and two holds, the stock registers a consensus “buy” with an average price target of $31.40. This implies an upside of 41.19%.

Is NMIH undervalued?

At its peak before the pandemic, NMIH traded just north of $34 a share. Although NMI has since issued additional shares, its EPS has nearly rebounded to pre-pandemic levels thanks to a growing portfolio of policies.

Yet, NMIH trades at a price-to-earnings ratio (P/E) of 9.8. For comparison, the P/E of the S&P 500 is greater than 31; the P/E of the insurance industry is 14.23.

To be fair, NMIH’s price-to-book ratio is 1.3, which is slightly higher than the industry’s (1.2).

So, is NMIH undervalued?

Wall Street analysts think so. It appears to be based on its fundamentals. But I’ll leave you with comments from Claudia Merkle, NMI’s CEO, to help you decide.

Looking forward, our outlook is positive. Industry volume is exceptionally strong with long-term demographic trends, supporting robust purchase demand and the experience of the pandemic reinforcing the value of home ownership. Credit performance is trending in a favorable direction with underwriting discipline remaining paramount across the mortgage market, record house price appreciation, providing a sizable equity buffer and an expanded and broadly applied government toolkit now available to assist borrowers through times of stress. Against this backdrop, we are executing on our plans and believe we are well-positioned to drive growth consistently, compound book value, and deliver for shareholders going forward.

Thanks for reading. Don’t forget to hit the heart button if you enjoyed today’s report.

If you haven’t subscribed already, you can do so here.