Good morning, investors!

Today, we’re following up on a company that’s had a pretty rough year: fuboTV.

If this is your first time with us, feel free to subscribe here. If you enjoy today’s newsletter, please hit the heart button at the end of the report.

Now, without further ado...

Why Is FUBO Stock Dropping?

“There can be no assurance that revenues from content based on [progamming] rights will exceed the cost of the rights plus the other costs of producing and distributing the content.” — an excerpt from one of fuboTV’s Risk Factors in its latest 10-K

When portfolios ride the bull and returns glow green, it’s easy to jump aboard growth stock bandwagons.

When bears come stampeding into the market and returns burn red, growth stocks often get annihilated.

fuboTV is getting annihilated.

But let’s back up. As you’ll recall from our DD report, FUBO offers live TV streaming services, particularly in the world of sports. The broader “cord-cutting” movement has benefitted platforms like fuboTV, which serve as a cost-effective alternative to traditional cable and satellite TV packages. And it shows in the company’s subscriber figures:

To better illustrate that 140% year-over-year increase, here’s a quarterly breakdown of paid subscriber growth.

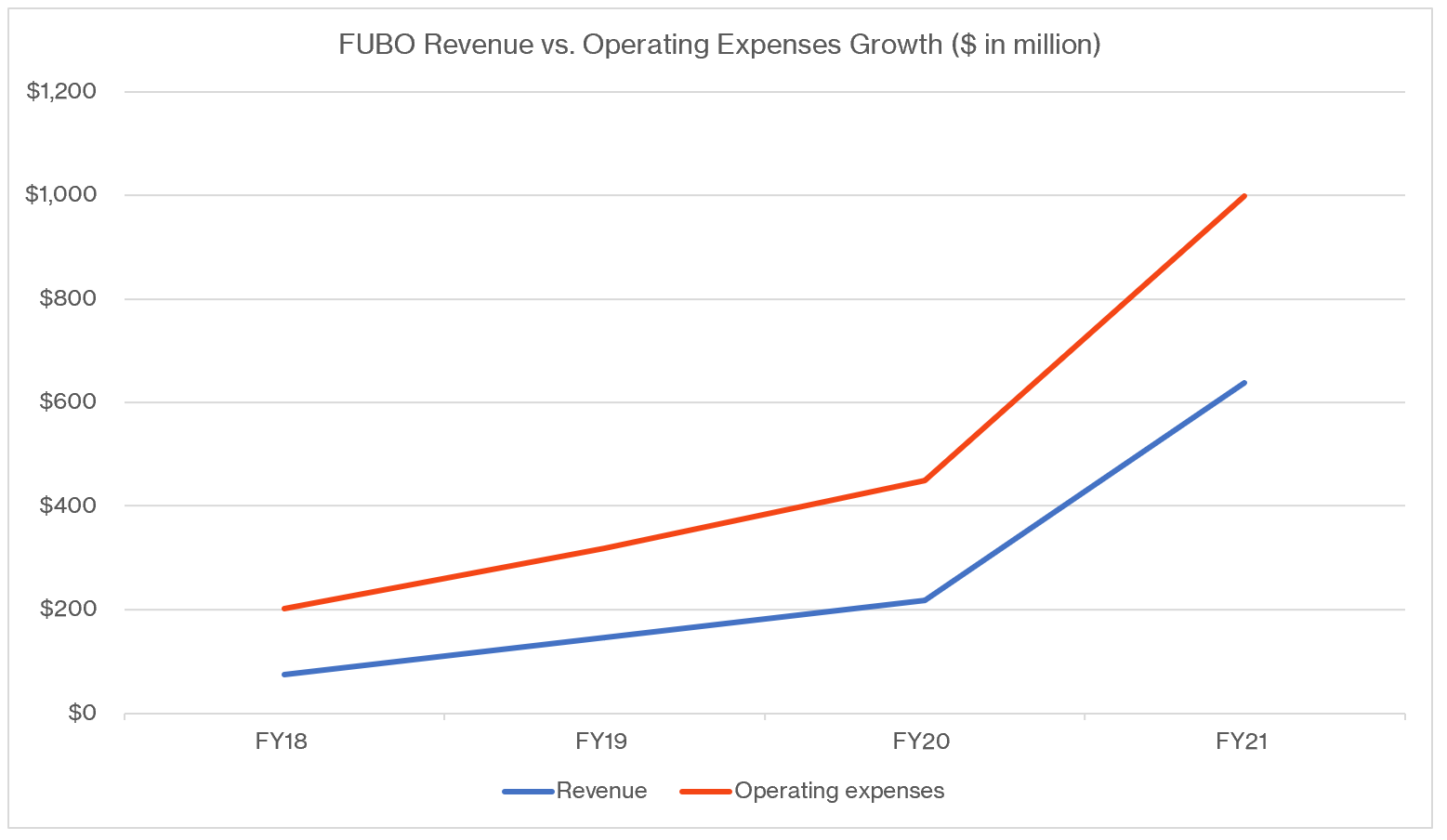

There’s no doubt that fuboTV is attracting subscribers to its platform, and that’s led the company to post record revenue growth as well. The issue is the cost of acquiring and maintaining those subscriptions.

fuboTV spent $142.4 million on sales and marketing last year. A large expense, but clearly, it worked. The more foreboding concern is the company’s subscriber-related expenses, which are essentially the fees fuboTV pays to air live programming. Live sports are expensive, so much so that these rights fees cost more ($593 million) than the revenue they generate ($564 million).

Long story short, fuboTV sells its primary product at a loss.

Add in the cost of actually running/growing the business, and you’ve got a sizable operating loss.

I even removed an asset impairment of $249 million in FY20 from Operating expenses.

Revenue is on the wrong side of that gap. Their operating losses have only continued to grow. That’s obviously a problem, one that investors don’t think fuboTV will solve.

Unfortunately, it could get worse before it gets better. The company added the following risk to its latest 10-K (emboldened for emphasis):

Risk: Our results may be adversely affected if long-term content contracts are not renewed on sufficiently favorable terms.

We enter into long-term contracts for both the acquisition and the distribution of media content, including contracts for the acquisition of content rights for sportingevents and other programs. As these contracts expire, we must renew or renegotiate the contracts, and if we are unable to renew them on acceptable terms, we may lose content rights or distribution rights.

Even if these contracts are renewed, the cost of obtaining content rights may increase (or increase at faster rates than our historical experience). Moreover, our ability to renew these contracts on favorable terms may be affected by consolidation in the market for content distribution, the entrance of new participants in the market for distribution of content on digital platforms and the impacts of COVID-19. With respect to the acquisition of content rights, particularly sports content rights, the impact of these long-term contracts on our results over the term of the contracts depends on a number offactors, including the strength of advertising markets, subscription levels and rates for content, effectiveness of marketing efforts and the size of viewer audiences. There can be no assurance that revenues from content based on these rights will exceed the cost of the rights plus the other costs of producing and distributing the content.

If rights fees rise, FUBO may not be able to overcome its mounting operating expenses. How can FUBO revamp this cash-burning, loss-generating business model? Management has expressed that they expect sales and marketing, G&A, and subscriber-related expenses to improve over time (in that order, but we’ll see). On the revenue side of things, the company has two areas of opportunity:

Advertising

Sports betting

As nettlesome as they can be, advertisements have a longstanding partnership with television. This is an area of opportunity for fuboTV because advertising is a high-margin business segment that could help lessen the company’s profitability gap. Fortunately for FUBO, as its subscribership has grown, so too has its ad revenue.

fuboTV management has kept its sportsbook trial results close to the vest, but they had previously predicted this business segment would generate 50% gross margins. Here’s the latest from CEO David Gandler:

We now have market access deals in 10 states, and we expect to launch fubo Sportsbook in additional markets soon. We believe entry into new markets will allow us to more effectively monetize our existing subscriber network. And we will create efficiencies in customer acquisition and retention and a deliberate, measured approach to growing our sportsbook with limited marketing spend.

We believe the ability to watch and wager within a single ecosystem is a feature that only fuboTV has brought to market.

Still, it remains to be seen if FUBO can scale these ancillary revenue sources to a point of materiality. They may be profitable in their own vacuums, but the bigger issue is whether FUBO can keep content spending and G&A expenses honest while it grows its subscriber base.

Do they have the liquidity to make it happen?

fuboTV operations burned through almost $193 million in 2021, however, thanks to a convertible notes issuance, the company has plenty of liquidity ($374 million of cash as of 12/31). So, at least in the near term, fuboTV should be able to execute its growth strategy. The more relevant question is, can the company turn that growth into profits and free cash flow?

Only time will tell.

As I mentioned in the September FUBO report, the company seemed pricy at $27.55, and I expected a better entry point in the coming months. Well, FUBO closed at $4.73 on Thursday. Assuming you believe in the company’s business model, that’s not a bad price tag for a growth stock that once traded in the $30s a year ago.

That said, the current macroeconomic climate isn’t exactly rosy. So, if you’re buying into FUBO, you’re likely holding for at least 3-5 years to see if the company can make good on its initiatives.

Wall Street’s consensus price target is $14.63.

News Roundup

For your reading pleasure:

Florida votes to dissolve Disney’s special district, eliminating privileges, setting up legal battle

Thanks for reading. Don’t forget to hit the heart button if you enjoyed today’s report.

If you haven’t subscribed already, you can do so here.