Good morning, investors!

Today, we’re going to check in with the go-to platform for spot-checking home values that are way beyond our spending power: Zillow.

If this is your first time with us, feel free to subscribe here. If you enjoy today’s newsletter, please hit the heart button at the end of the report.

Also, a quick note: I’ll be taking a brief respite from Due Diligence next week, as I’ll be traversing the Bourbon Trail in Louisville.

Without further ado…

Zillow (ZG)

On March 19, we released our Zillow Due Diligence report. Our analysis came shortly after Zillow ballooned to $212 a share after entering the year a hair under $100 (and up from a pandemic low of $26.49). The recent housing market boom was largely responsible for the share price rally.

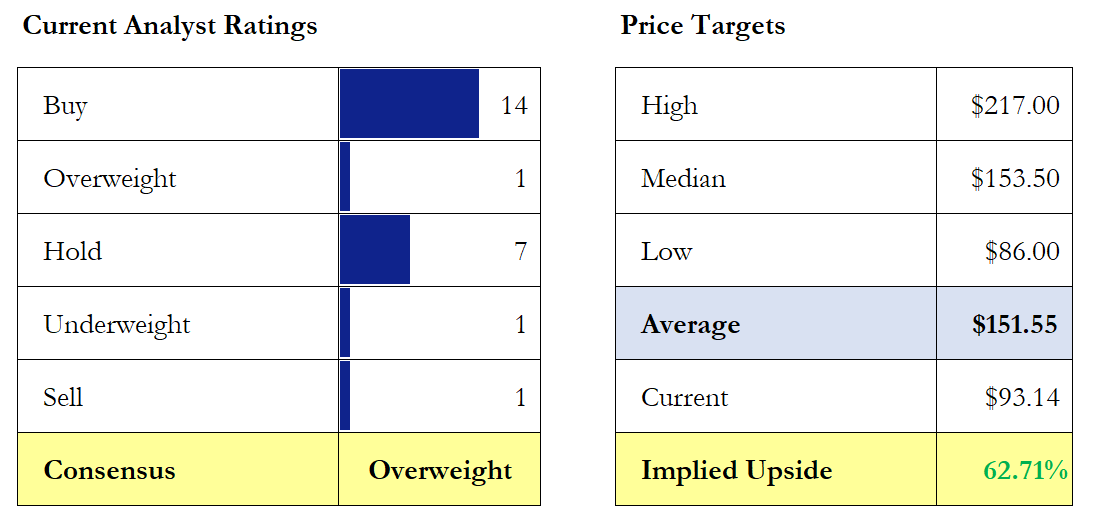

Since then though, Zillow’s share price has shed some weight, dropping to $93.14 as of Thursday.

There are a number of reasons. Many early holders likely elected to recognize their gains. Recent earnings didn’t wow investors. Lastly, the prospect of rising interest rates hasn’t helped matters either, as this tends to slow home purchases and new mortgages.

However, a more recent hurdle poses to do more damage to Zillow’s growth trajectory.

Zillow hits pause on home purchases

Zillow’s positioning as a digital solution in a largely physical industry has been appealing for quite some time. From a profitability perspective, advertising has been its moneymaker. But, in 2018, Zillow sought to extend its operations, dipping its toes into the home-flipping business when it released Zillow Offers.

Per our March report:

Launched in 2018, this program has three stages: (1) Zillow provides cash offers to homeowners; (2) Zillow’s renovation team repairs acquired homes; and (3) Zillow lists and sells the home back on the market for a higher price.

For home shoppers, it’s a convenient service. But, from a business perspective, Zillow is still working out the kinks.

Earlier this week, Zillow announced its plan to stop buying homes for the remainder of 2021. Instead, management will prioritize clearing its current backlog of house purchases.

Per COO Jeremy Wacksman:

"We're operating within a labor- and supply-constrained economy inside a competitive real estate market, especially in the construction, renovation and closing spaces. We have not been exempt from these market and capacity issues and we now have an operational backlog for renovations and closings. Pausing new contracts will enable us to focus on sellers already under contract with us and our current home inventory."

Although Zillow Offers generated $1.4 billion of revenue in the first half of 2021, its business unit had a net loss of $117.8 million. The good news is that Zillow’s IMT segment (i.e., ad revenue) is doing quite well. Through the first six months of the year, Zillow’s IMT segment turned a profit of $277.1 million, more than offsetting losses elsewhere.

Financials aside, this may shed light on a more concerning aspect: scalability. Even with labor and materials shortages, the fact that Zillow had to halt purchases does not bode well for scaling this service. That’s not to suggest it can’t be done, it’s just something to be wary of going forward.

Is Zillow undervalued?

Most Wall Street analysts seem to think so (however, the same was true in March). As of today, 14 of 24 analysts covering the company consider it a “buy.”

Thanks for reading. Don’t forget to hit the heart button if you enjoyed today’s report.

If you haven’t subscribed already, you can do so here.