The Big Picture

It’s a tough time to be in the travel business, but that hasn’t stopped Airbnb’s stock price from ballooning to as high as $216 after listing at $68 in December. Investors are enamored with Airbnb’s growth potential. Plus, the company’s business model proved resilient in 2020, and well-timed financing activity flushed its balance sheet with cash. But it still faces a number of hurdles — most notably, travel demand and restrictions.

Is now the time to book a long-term stay with ABNB?

The Business

In 2007, two hosts welcomed three guests into their San Francisco home, and Airbnb was born. Since then, Airbnb has grown to 4 million hosts, who have welcomed over 800 million guests in roughly 100,000 cities across almost every country in the world. Unlike traditional hotel and lodging services, Airbnb’s hosts are everyday people willing to open up their homes to travelers. The intended result is a more intimate and authentic travel experience, often at a discount compared to commercial lodging options. Listings include houses, cabins, treehouses, boats, castles, and even luxury villas.

Airbnb generally classifies its hosts into one of two categories: individual and professional. Individual hosts list their private rooms, primary homes, or vacation homes directly on Airbnb through its website or mobile apps. Professional hosts often run property management or hospitality businesses, using the company’s platform to list their properties. Although the company is based in the United States, Airbnb is firmly entrenched as a global company with 86% of hosts located outside of the U.S.

Shortly after the COVID-19 pandemic erupted in the United States, Airbnb adjusted to the evolving market to encourage longer-term stays, updating its website to promote this functionality. The shift came at a time when remote work became the norm. At the time, about 80% of hosts accepted long-term stays and roughly half of active listings offered discounts for stays of a month or longer.

In addition to connecting guests with travel destinations all over the world, Airbnb also offers deeper value via Airbnb Experiences: activities hosted by local experts for guests. Before the pandemic, guests could book these experiences via the company’s website/app. Once the pandemic limited travel, Airbnb paused this initiative and pivoted to Online Experiences, which function in a similar way but digitally. For example, the World's Top Coffee Masterclass is an Online Experience hosted by coffee fanatics that analyzes the qualities of a good cup of coffee.

Host Endowment Fund

In October 2020, Airbnb established a Host Endowment Fund to reward, support, and incentivize its community of hosts. Once the value of the endowment exceeds $1 billion, the company will start to invest the funds in the host community via education grants, emergency funds, new products to support hosts, and an annual payout to a select group of hosts who most advance Airbnb’s mission.

Growth Strategy

One of the primary reasons Airbnb is an exciting company is its growth potential. Even though the travel giant is already well established across the globe, it still has a massive opportunity for expansion. Airbnb’s long-term growth strategy revolves around six company strengths:

Unlock more hosting

Grow and engage the guest community

Invest in the Airbnb brand

Expand its global network

Innovate the company’s platform

Design new products and services

More hosts

Airbnb’s travel offerings go as far as its hosts do. If there are 4 million hosts, then there are at least 4 million potential places to stay. If someone opens up their beach-side shack in Fiji, well then Airbnb can add it to the destination list. The only way to accommodate more guests is to add more hosts.

Airbnb is specifically focused on adjusting to remote-work trends and long-term stays. The company emphasizes the importance of educating its host community and providing them with the necessary tools to enhance the guest experience.

More guests and engagement

It’s a simple formula: more guests = more service fees. And, if Airbnb has its way: more happy guests = more service fees and brand advocates.

The pandemic fundamentally changed remote-work dynamics and travel; Airbnb believes it can leverage its market position to take advantage of this change. While the company doesn’t publicly specify, Airbnb believes it can create products based on changing behaviors to not only attract more guests but also allow them to connect with each other.

More marketing

Last year wasn’t an ideal time to market travel services. Unsurprisingly, Airbnb reduced sales and marketing spend by nearly 28%. However, Airbnb still maintains one of the most recognizable brands, and they intend to capitalize on this strength during new product/feature launches.

More expansion

It’s hard to imagine a global company expanding even more, but the company plans to increase its presence in lower penetration markets, including India, China, Latin America, and Southeast Asia. The biggest (and most obvious) roadblock is working with local governments and regulatory bodies to ensure short-term rentals are permissible.

More innovation, products, and offerings

And more generic buzzwords. They plan to improve the host and guest experience by making the Airbnb platform more accessible and appealing.

Key Business Metrics

Airbnb tracks and reports two metrics: (1) Nights and Experiences Booked and (2) Gross Booking Value. These aren’t official, GAAP-compliant metrics, but the company uses them to measure performance, identify trends, formulate projections, and make strategic decisions.

Note that values are in millions

Nights and Experiences Booked

As the name implies, this statistic measures the sum of (a) total nights booked for stays and (b) seats booked for experiences, net of cancellations and alterations. To date, substantially all of the company’s bookings have been derived from nights — which isn’t much of a concern considering experiences are a newer and lesser-known offering. The company believes it’s a key measure of the platform’s scale since each booking represents a single transaction.

Bookings were down 41% in 2020; the company was hit the hardest in the second quarter when bookings declined 67% year-over-year. This continued into the third and fourth quarters, as the company experienced 28% and 39% declines, respectively, from the prior-year periods. However, the company noted that domestic and short-distance travel improved in the second half of the year — an early indicator of a travel rebound.

Gross Booking Value

Gross Booking Value (“GBV”) represents the total dollar value of Airbnb’s bookings, including host earnings, service fees, cleaning fees, and taxes — net of cancellations and alterations.

Like bookings, GBV was down 67% in the second quarter of 2020; however, the third and fourth quarters only dropped by 17% and 31%, respectively. The company attributes this to a shift toward North American bookings.

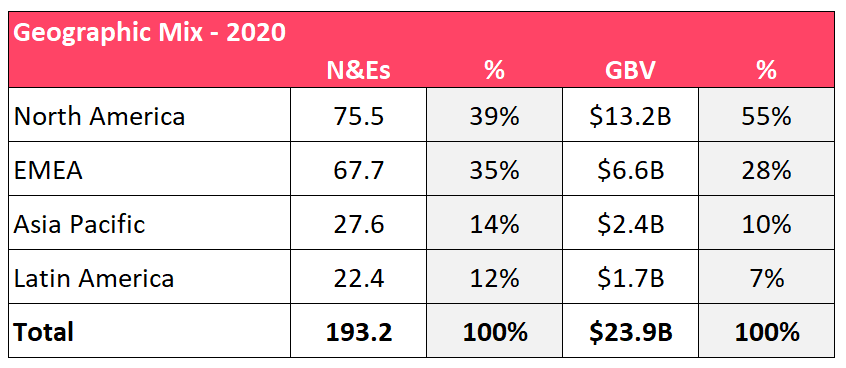

Geographic Mix

Airbnb is a global company, but North America accounted for more than 50% of GBV in 2020. The table below outlines Airbnb’s Nights and Experiences Booked and GBV by region. Note that EMEA represents Europe, the Middle East, and Africa.

North America's activity helped minimize losses in FY20. Going forward, the company plans to expand its operations in less-penetrated regions like the Asia Pacific and Latin America.

The Narrative

The pandemic crushed tourism across the globe. Shocker, travel restrictions are bad for the travel industry. Airbnb was not impervious to the economic fallout.

The company’s operations were initially impacted in late January 2020, when COVID-19 surfaced and spread around China. The virus continued to spread and surge around the world in all major territories. (You know where this story goes.) This prompted Airbnb to raise $2 billion of term loans in April to reinforce liquidity and protect the company’s operations. Further, the company reviewed its cost structure and took substantial actions to minimize adverse business impacts, including:

Suspending almost all discretionary marketing spending

Reducing full-time employee headcount by 25%

Suspending all facilities build-outs and reducing capital expenditures

Pausing investments and initiatives in newer areas like transportation and content

Airbnb believes these actions will result in improved operating leverage in the post-pandemic world. The biggest questions coming out of the pandemic are:

Will travel demand rebound?

Does the company have adequate liquidity to sustain more losses if demand doesn’t rebound?

While the company expects early 2021 results to remain suppressed due to the pandemic, it believes the widespread distribution of vaccines poses a promising opportunity for travel recovery. According to an Airbnb survey in December 2020, 54% of respondents said they have either already booked a trip, are currently planning to travel, or expect to travel in 2021. That percentage will likely increase as more people get vaccinated. However, no one can confidently or definitively say when travel demand will return to pre-pandemic levels.

That leads us to our second question: can the company outlast more losses? As you’d expect, the pandemic burned through a hefty chunk of Airbnb’s cash; free cash flow was ($667) million in 2020. However, even though we aren’t fortune tellers, the company appears well-positioned from a liquidity perspective thanks to recent financing activity.

IPO

On December 14, 2020, Airbnb completed its IPO, which raised $3.7 billion in net proceeds. So, despite the negative cash flow, Airbnb had $7.7 billion of cash and cash equivalents at the end of 2020 — compared to about $2 billion of debt.

Speaking of debt...

Convertible Notes

Airbnb announced in early March that it’s offering $2 billion of convertible notes to institutional investors at a 0% interest rate. Convertible notes enable investors to exchange debt into shares at a predetermined price (in this case, the initial conversation is 3.4645 shares per $1,000, or $288.64 per share).

The proceeds from the notes (along with some cash) will repay the company’s existing indebtedness. That means the company will effectively eliminate its interest expense. To give you an idea of annual savings, Airbnb paid about $130 million in interest last year.

While the IPO proceeds flushed the company with cash, the convertible notes reduce cash outflows going forward. Coupled together, these financing activities bolster the company’s financial health.

Regulatory Issues

Beyond the public health crisis, the company’s primary growth roadblock is regulatory restrictions. In other words, Airbnb must comply with local ordinances to enable hosts to provide housing rentals to guests. Considering Airbnb operates in thousands of cities with varying laws, it’s not a simple issue to manage and overcome. For instance, many large cities limit the number of nights permitted for short-term rentals; as you can imagine, that limits both the host’s and the company’s income potential.

That said, no single city represented more than 1.1% of FY20 revenue (prior to incentive/refund adjustments). So, if a particular city bans short-term rentals and effectively exiles Airbnb’s operations, the company wouldn’t see a material revenue dip. But, then again, if state regulators or federal governments pose widespread bans, it’s a different story.

The Competitors

Although it was a novel idea to connect travelers with personal homes instead of commercialized lodging, Airbnb still has a lot of competitors — including online travel agencies, travel listing websites, hotel chains, search engines, and short-term rental companies.

So, it’s a cutthroat market. Note: the following table could include many more competitors.

In our opinion, the number that jumps off the page is market capitalization; ABNB maintains a significantly larger market share than each of these competitors — including BIDU, a China-based search engine that generated 4.8x as much revenue on a trailing twelve-month basis.

Excluding BIDU, EPS was negative for each of these companies (keep in mind ABNB looks worse than it is due to stock-related comp).

The High-Level Finances

Since ABNB only recently went public, we don’t have access to financial results before 2018.

Note that all dollar amounts are illustrated in millions.

Revenue

Airbnb’s revenue is pretty straightforward: service fees charged to customers (net of incentives and refunds). The company charges a fee as a percentage of each booking’s price, which varies based on duration, geography, and host type. Incentives and refunds totaled $221.5 million, $274.5 million, and $384.2 million in 2018, 2019, and 2020, respectively. These amounts represented 6%, 6%, and 11% of revenue. As you can imagine, the pandemic spurred the near-doubling of refunds in 2020.

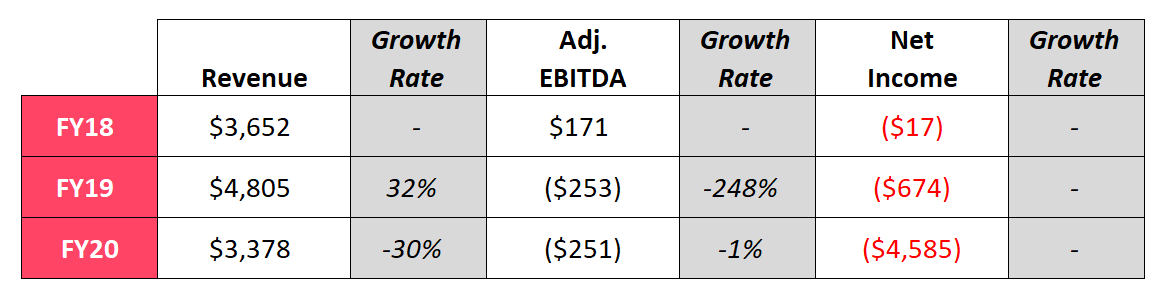

ABNB experienced a 30% revenue decline from FY19 to FY20. Considering the circumstances, that’s not a surprise.

What is a surprise? The company generated positive operating income over the second half of 2020, excluding stock-based compensation expenses (which are non-cash). In other words, the company proved it can successfully manage costs in even the most severe downside scenarios.

ABNB’s revenue peak in FY19 was driven by a 33% increase in the number of check-ins related to Nights and Experiences Booked. The company launched a big marketing campaign in 2019, and, based on the numbers, it worked.

EBITDA

EBITDA (earnings before interest, taxes, depreciation, and amortization) is a metric used to gauge a company’s operating performance. A company’s operations can appear worse due to certain non-cash expenses, such as depreciation and amortization.

We’ve illustrated Airbnb’s reported Adjusted EBITDA, which also accounts for (a) stock-related compensation (a non-cash expense), (b) lodging tax reserves, and (c) acquisition-related impacts (a relatively immaterial amount that only impacts FY20).

Surprisingly, ABNB’s Adjusted EBITDA in FY20 nearly matched the previous fiscal year; however, the company still exhibited negative results. That was expected since the pandemic annihilated the tourism industry. In fact, one could easily argue that ABNB’s operating results are relatively successful, all things considered.

If you’re skeptical of the EBITDA decline from FY18 and FY19, we get it — we were too. The primary driver was increased advertising expenses ($474.5 million in FY18 versus $712.6 million in FY19).

Net Loss

Although the company’s losses look like their snowballing, ABNB’s net loss in FY20 is very misleading. The $4.6 billion loss was primarily driven by two major non-cash expenses: (1) stock-based compensation expense of $3 billion and (2) a liability increase of $868.5 million related to the reevaluation of warrants held by the company’s term loan lenders.

The stock-based compensation related to the vesting of restricted stock units (“RSUs”), which were primarily issued to Airbnb employees. In essence, employees get shares of the company once two conditions are met: (a) employees work for a certain amount of time and (2) the company goes public. Well, Airbnb went public in December 2020, triggering the vesting conditions of its RSUs. This form of compensation doesn’t directly cost the company money, but it does dilute shareholder value via the issuance of more shares.

The warrant liability is another non-cash expense. The company gave its lenders warrants to purchase almost 8 million shares of stock. The fair value of these warrants totaled $985.2 million at year-end, representing an increase in liability of $868.5 million. At some point, these lenders could exercise their right to purchase shares of ABNB at roughly $28 per share — or reach a cash settlement. Hence, the liability.

All of that said, even if you negate these non-cash expenses, the company still incurred losses last year. While the travel industry is expected to rebound, profits aren’t guaranteed by any means.

The Primary Strengths

Host community. Airbnb’s host community now exceeds 4 million people across roughly 100,000 cities. It’s clear that the company intends to continue investing in its hosts so that they, in turn, can provide memorable experiences to their guests. The Host Endowment Fund is a prime example of this intention.

Capital. Thanks to a $2 billion term loan in April 2020 and $3.7 billion of IPO proceeds in December 2020, Airbnb is in a strong liquidity position — even if operations continue to generate negative cash flow in the near term.

Resilient business model. The pandemic suppressed operating results, but domestic travel showed signs of life in the second half of the year. The company noted that booking durations began to increase as people adjusted to remote working environments. This benefits hosts and the company, as longer stays generate more service fees.

In addition, throughout 2020, Airbnb’s active listings remained stable at roughly 5.6 million despite booking declines — a good sign that hosts are still actively using the platform.

Travel rebound. Since a travel rebound isn’t guaranteed, this is both a strength and a risk. On the glass-half-full side, the company’s operations didn’t suffer as much as expected last year. The company endured arguably the biggest blow possible and survived, so it seems reasonable to believe 2021 results would be better.

Expansion opportunities. While the company has regulatory hurdles to overcome, Airbnb has targeted certain geographic regions for increased penetration — such as the Asia Pacific and Latin America.

The Primary Risks

Travel rebound (or lack thereof). Airbnb isn’t out of the woods yet. Even though vaccines are becoming widely available, that won’t necessarily incline people to travel. Airbnb has billions of dollars to cover potential losses — but its liquidity won’t last forever if people don’t start collectively traveling again.

Regulatory challenges. Navigating national, state, local, and foreign laws across all host cities is an onerous task. Certain regulations against short-term rentals and home-sharing have and can continue to limit Airbnb’s ability to penetrate certain markets. If, for example, China outright bans Airbnb’s platform within its borders, that would hinder the company’s financial results.

Legal liability. Along the same lines, complying with applicable laws (which, the company notes, are often ambiguous) can be burdensome. Airbnb has and could continue incurring penalties and facing lawsuits as a result of legal disputes.

Failed offerings and initiatives. Researching and developing new product features and initiatives is very expensive. The company hasn’t disclosed future offerings, but — no matter what they are — they aren’t guaranteed to succeed. If these offerings and initiatives fail, the company’s liquidity would be adversely affected.

The Street’s Opinion

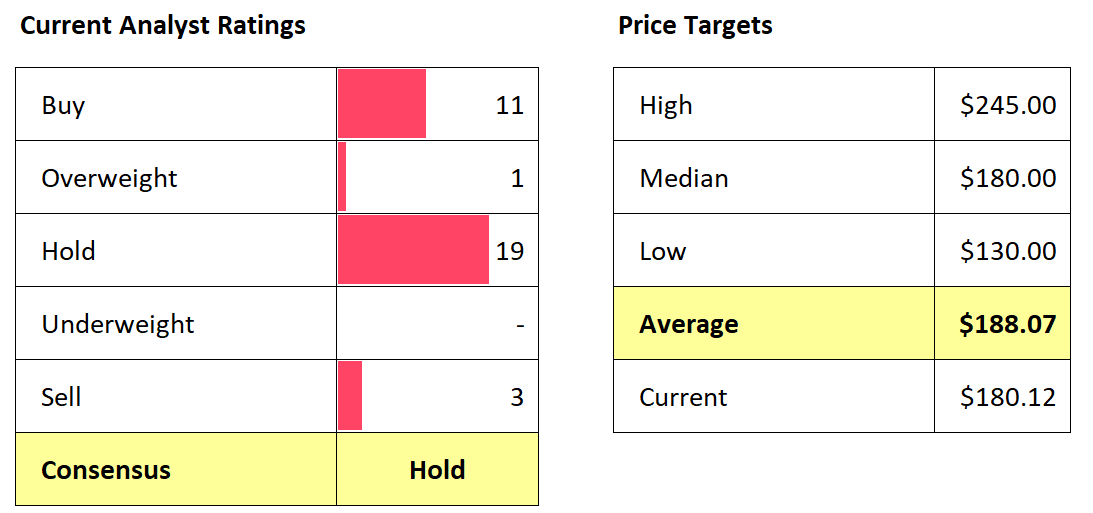

ABNB is a popular stock to track; 34 analysts issue ratings for the company. Most analysts (19) currently rate ABNB as a “Hold.” However, there are 12 analysts that are optimistic with 11 “Buy” ratings and 1 “Overweight” rating. The remaining three issued “Sells.”

The average price target ($188.07) is relatively in line with the stock’s current price ($180.12)

Recent News

Time to Book Your Next Investment?

It’s hard not to get excited about Airbnb’s growth potential. It’s established footholds in major markets all over the world. It appeals to younger demographics. Its balance sheet is flushed with capital. Plus, the company’s brand and platform enable it to experiment with new products and establish additional revenue sources.

However, none of that matters if the travel industry takes another major blow from the pandemic. On top of that, Airbnb still faces abundant legal challenges, which can be costly and inhibiting. So it’s not exactly smooth sailing from here on out.

We’re optimistic about Airbnb’s future — especially a post-pandemic one. So much so that we actually own shares of ABNB. (For the record, we aren’t financial advisors and we aren’t persuading or dissuading you from investing in ABNB.)

It’s impossible to predict how the travel industry will react and adapt to a post-pandemic world. So, keep an eye on (1) any studies or research about tourism that surface this year to gauge travel demand; (2) Airbnb’s platform for new features and product offerings, which could help diversify the company’s revenue mix; (3) Airbnb’s penetration into Asia and Latin America, which are key regions within the company’s growth strategy; and (4) any news related to laws and regulations that would adversely impact the company’s business model.

Sources

Update on the Airbnb Host Endowment and Our Commitment to Communities

Airbnb rolls out new features aimed at its next big bet: longer-term stays (TechCrunch)

Want our free stock coverage in your inbox? Sign up now so you don’t miss our reports.