The Big Picture

Much like Gamestop, the short-sellers are gunning for AMC — especially after the pandemic restricted movie attendance across the globe. Despite horrendous operating results last year, social momentum continues to keep the company’s share price afloat. AMC took advantage by issuing enough new equity to almost fill a couple of Brinks trucks.

But liquidity concerns still loom thanks to expensive debt and rent obligations totaling multiple billions of dollars.

The film industry is still in shambles, but there’s a glimmer of hope on the horizon thanks to the widespread distribution of COVID-19 vaccines, which is expected to rejuvenate the movie business. Movies aren’t going anywhere — but will AMC be around to exhibit them?

Is this AMC’s grand finale?

The Business

AMC Entertainment Holdings, Inc. (AMC) is the world’s largest theatre operator. The company’s history spans multiple generations, dating back to its founding in 1920 in Kansas City, Missouri. That history led to a sizable network of theatres across the globe. As of December 2020, AMC owned, leased, or operated 950 theatres and 10,543 screens in 14 countries, including 590 theatres and 7,668 screens in the U.S. and 360 theatres and 2,875 screens in European markets and Saudi Arabia. Fun fact: roughly 49% of the U.S. population lives within 10 miles of an AMC theatre.

A lot goes on behind the scenes of a movie’s lifespan (pun absolutely intended) — such as production, distribution, promotion, and exhibition. (I only know about the process because I covered film & TV content companies during my banking days.)

AMC exhibits films — it doesn’t produce, edit, or own any of the content it shows. Instead, the company licenses “first-run” films (i.e. new films releasing to the public for the first time) from major film companies and smaller independent studios/distributors. It purchases the exclusive rights to release and show films for set windows of time (e.g. 31 days). Then the rights revert to the distributor, who will then sell the film to other viewing channels (like streaming platforms).

AMC organizes its revenue sources into three segments:

Box Office Admissions. The ticket purchases by movie-goers visiting AMC’s theatres. Since it “rents” the content it exhibits, AMC splits box office admissions with each film’s distributor. The split varies depending on the film and theatre. This category accounted for 57.3% of FY20 revenue.

Food and Beverage. Traditionally, F&B includes popcorn, soft drinks, candy, and hot dogs, but AMC also offers alternatives like alcohol, coffee, made-to-order meals, and healthier snacks. However, the company adopted a simpler concession menu after the pandemic. This category accounted for 29.2% of FY20 revenue.

Other Theatre Revenue. It’s essentially “everything else,” including on-screen advertising (e.g. previews), online ticketing fees, income from gift cards, and packaged tickets. This category accounted for 13.5% of FY20 revenue.

Loyalty Program

AMC’s loyalty program (AMC Stubs) enables members to earn rewards, receive discounts, and participate in exclusive members-only offerings and services. The AMC Stubs program consists of three tiers:

AMC Stubs A-list: monthly paid membership

AMC Stubs Premiere: annual paid membership

AMC Stubs Insider: the free membership option

Launched in June 2018, the A-list tier of the program offers subscribers admission to movies at AMC theatres up to three times per week, including multiple movies per day and repeat visits to already seen movies. A-list subscribers also gain access to other premium offerings, like online booking for reserved seating. Monthly subscription fees range between $19.95 and $23.95, depending on the geographic market.

Premiere offers rewards like upsized popcorn and fountain drinks or exclusive access to discounts (e.g. “Discount Tuesdays”). Guests accumulate progress toward rewards with frequent patronage of AMC theatres (e.g. $5 rewards or free large popcorn). The Premiere membership costs $15 per year.

At the end of 2020, the AMC Stubs program had 23,300,000 member households enrolled across its three tiers. These members represented roughly 45% of U.S. theatre attendance in 2020. Outside of the U.S., AMC maintains more than 11,400,000 members across its various international loyalty programs.

Commentary: Before the pandemic erupted, the A-list subscription model had been a huge success, gaining 800,000 subscribers in the program’s first year. When the company temporarily suspended theatre operations due to the outbreak, it paused A-list subscription payments, allowing members to keep their plans for free during a sparse film release schedule. Currently, A-list members have until July to resume their plan or cancel.

Studio Partners

AMC has longstanding partnerships with the world’s largest film companies, such as Sony, Disney, Universal, Warner Bros., Paramount, and Lionsgate. These companies accounted for 80% of AMC’s U.S. admissions revenue in FY20.

Some good news: Amidst the pandemic pandemonium, the company entered a multi-year agreement with Universal to maintain exclusive theatrical viewing windows. After the windows close, Universal has the option to distribute film content across PVOD platforms (premium video on demand); AMC will also share in the revenue streams generated from PVOD opportunities.

Some bad news: Warner Bros. is putting its entire 2021 film slate on HBO Max as they debut in theatres. This eliminates theatrical exclusivity; if people want to see a particular Warner Bros. movie, they don’t have to make a trip to a theatre. That’s bad news for AMC.

Wanda ownership

The Dalian Wanda Group Co. (“Wanda”), a massive Chinese conglomerate, has been AMC’s largest and most involved shareholder since it acquired AMC in 2012. As of December 31, 2020, Wanda owned roughly 23% of AMC’s outstanding common stock and controlled about 47% of voting power. However, Wanda reduced its stake and voting power in AMC to 9.8% as of March 3.

AMC stated that Wanda still maintains significant influence over the company (and it does, considering Wanda still owns two board seats); however, Wanda’s actions are not exactly a vote of confidence in AMC’s current operations and future outlook.

Business strategy

It almost feels futile to discuss the company’s long-term strategy, considering they’ve suspended growth initiatives and are prioritizing short-term solvency instead. But let’s check the box anyway before we get to the juicy stuff.

AMC’s long-term strategy:

Transform AMC into a world-class leader in customer engagement

Deliver the best in-person experience while at AMC theatres

Expand and strategically close underperforming theatres

From a short-term outlook, the company is reliant on external factors: (1) increased attendance (which hinges on the pandemic), (2a) increased film production, and (2b) theatrical releases instead of straight-to-streaming or other channels. Until those factors show signs of life, the company’s long-term strategy is on hold.

The Narrative

Despite AMC’s rich and lengthy history, we’ll focus on the company’s most recent chapter: the COVID-19 chronicles. On March 17, 2020, AMC temporarily suspended its theatre operations across the globe. International operations resumed in a limited capacity in June, and domestic theatres followed suit in August. When COVID-19 resurged in the fall, the company was forced to temporarily suspend some international operations again.

Over the course of the year, AMC shaved its labor force by a startling 35.6% (38,872 employees to 25,019). The company’s overall U.S. theatre attendance declined by 92.3% in the fourth quarter of 2020 relative to the prior-year period.

In short, it was a disastrous year for AMC — and the rest of the film and TV industry. Production companies stalled filming and delayed releases beyond 2020 — or moved them to non-theatre channels (e.g. streaming platforms like Netflix or HBO).

(I mean, just look at this running list of pandemic-impacted films and programs.)

Per the National Association of Theatre Owners, box office revenues declined nearly 81% in 2020. Last year was an anomaly — no doubt about it — but it’s a long road to recovery.

Revenue and attendance figures are in millions.

Thankfully, vaccines are now being widely distributed, which is expected to rejuvenate attendance and the broader film industry. However, it’s not an instantaneous process. AMC still faces a daunting liquidity obstacle.

Liquidity Plans

AMC is in a liquidity pickle — and that’s putting it super delicately. On its last earnings call, company management noted that AMC’s monthly cash burn was about $124 million in the fourth quarter. The company’s annual report outright states the following: “Our cash burn rates are not sustainable.”

The company has ambitious liquidity plans; we’ve highlighted the three major ones:

More equity issuances.

Landlord negotiations.

Creditor discussions.

More equity, please.

AMC took advantage of its social status as a “meme stock” by raising roughly $870 million through the issuance of about 278 million shares over the last four months. The company notes that it could pursue more equity issuances in the future to combat liquidity problems. So long as the company’s share price remains elevated, it can tap the markets for more capital (diluting its share price in the process, of course).

More IOUs, please.

The company took actions to mitigate COVID issues, such as limiting non-essential capital expenditures, halting dividends and stock repurchases, reducing corporate salaries, and furloughing employees. However, most importantly, AMC is working with its landlords to manage its rent expenses — which are hefty.

Last year, to offset suspended operations, AMC negotiated with its landlords to defer rent obligations. In essence, they wrote a bunch of IOUs.

Well, those IOUs are due soon.

AMC managed to defer $450 million of rent obligations during the pandemic, but they start becoming due this year. The company is actively negotiating for rent abatements or additional deferrals to remain liquid.

Sure, AMC could manage to reduce its total obligation, but it’s hard to imagine the company’s landlords eliminating or even deferring rent much further — especially considering the company just raised north of $1 billion from equity and debt issuances, which is public information.

In short, even with revitalized attendance, the company’s future cash flows are already obligated to its landlords and creditors. Speaking of creditors...

Let’s talk it out.

At the end of 2020, AMC had $5.8 billion of long-term debt — expensive debt that will further restrict future cash flows. The company’s 10-K also notes that even if its operations return to pre-pandemic levels, the company will still need to engage in discussions with its creditors to substantially reduce its leverage. One solution they’ll likely propose (which they mention) is converting debt to equity.

In essence, the company is attacking potential insolvency with dump trucks of new shares in the form of stock issuances and convertible debt.

The Competitors

AMC is the world’s largest theatre chain, but that’s not exactly a coveted title right now, considering (a) the lack of movies (and, thus, ticket sales) and (b) the sizable financial obligation that comes with leasing and operating theatres. However, there are other theatre chains out there, including Cinemark, IMAX, and Regal Entertainment (which isn’t publicly-traded).

Data as of 3/25/2021

There are a few glaring differences between AMC and its competitors. First, it trades for half the price — but that’s not shocking based on everything we mentioned above. Next, look at that average trading volume — it dwarfs Cinemark and IMAX. (That’s the power of social momentum.) Lastly, the company’s earnings per share are horribly bad, but it’s clear that the struggle is universal among film exhibitors.

The High-Level Finances

Note that all dollar amounts are illustrated in millions.

Revenue

In 2016 and 2017, AMC made major acquisitions of existing film exhibitors to expand its network of theatres/screens. As you can see, these acquisitions significantly boosted the company’s revenue (a 57% bump in FY17).

However, the largest and most pressing issue going forward is how the company will continue adapting to the pandemic-altered landscape. As we mentioned, AMC is burning through cash at a scary fast clip. If its box office admissions don’t exceed expectations (and, even then, that might not matter), the company will be in a major liquidity bind within the year.

EBITDA

EBITDA (earnings before interest, taxes, depreciation, and amortization) is a metric used to gauge a company’s operating performance. A company’s operations can appear worse due to certain non-cash expenses, such as depreciation and amortization.

We’ve adjusted AMC’s EBITDA to also account for significant non-cash impairments, which are primarily related to the impairment of goodwill. AMC evaluated its business segments by analyzing cash flow projections and determined their fair market values were less than the company’s books stated.

Regardless of the add-back, AMC’s EBITDA drastically declined in 2020 due to suspended operations and the pandemic’s economic fallout. Even though theatres are resuming limited operations, we don’t expect operating results to recover for quite some time — if ever.

Net Loss

Before the calamity of 2020, AMC had traditionally been a profitable business. Margins weren’t high, but it was profitable nonetheless. (The company’s FY17 net loss was primarily a result of significant levels of acquired depreciation when the company bought Nordic Cinemas.)

While much of the $4.6 billion loss was driven by $2.3 billion of non-cash goodwill impairments, the impairments themselves are still major concerns. Essentially, the company analyzed expected future cash flows of its domestic and international theatres and made a grave realization: the company’s market value was vastly beneath what it was entering 2020.

The Primary Strengths

Market share. AMC has a vast network of theatres (which, as we mentioned, is arguably a weakness too) across the world’s major film markets. So, if there’s a company that’ll benefit from more people going to movies in 2021, it’s AMC.

Loyalty program. Based on its loyalty program (AMC Stubs), the company estimates that its consumer database is approximately 50 million people. Further, the company’s A-list subscription tier showed promise before the pandemic ceased monthly payments. Needless to say, customer loyalty is only a viable strength if AMC has theatres open and films to show. Reports regarding renewed A-list subscriptions will be telling.

Equity inflows. My, oh my, did AMC take advantage of its social media momentum, or what? The company raised roughly $870 million through the issuance of about 278 million shares over a 4-month stretch. Paired with new debt issuances, the company has stated that it has enough liquidity to comply with its creditors’ liquidity covenants until March 2022.

The Primary Risks

Cash burn. AMC has been frank about its financial situation: its current cash burn rates are unsustainable. The company’s monthly cash burn was about $124 million in the fourth quarter. If it doesn’t start generating cash flow soon, the company’s outlook will remain bleak.

Massive obligations. Between its long-term debt and lease obligations, AMC owes its creditors and landlord billions of dollars. Interest, rent, maintenance Capex — these mandatory expenses are climbing faster than the company’s currently generating cash.

Stay afloat. Historically, AMC’s primary method of growth has been capital-intensive projects like strategic acquisitions and revamped F&B services. Debt hinders the company’s business to pursue business-growing initiatives (which the company has outright expressed). In other words, AMC isn’t striving for increased profit margins — it’s in survival mode.

Dilution. To put out the liquidity fire, AMC issued a lot of shares. While that keeps the business going, that’s bad for shareholder value. As of March 3, AMC had more than 450 million outstanding shares of common stock. About 15 months earlier, it had roughly 104 million outstanding shares. Simply put: more shares = less value per share. Yet, social momentum has kept the stock price up.

Susceptible to external factors. AMC is reliant on consumer confidence and society’s desire to return to the movies. Further, as some film companies have already elected to do, many films could continue skipping theatrical releases altogether — which cuts AMC out of the picture. Based on its extension of A-list subscription renewals, the 2021 film slate might not pick up until mid-July or later.

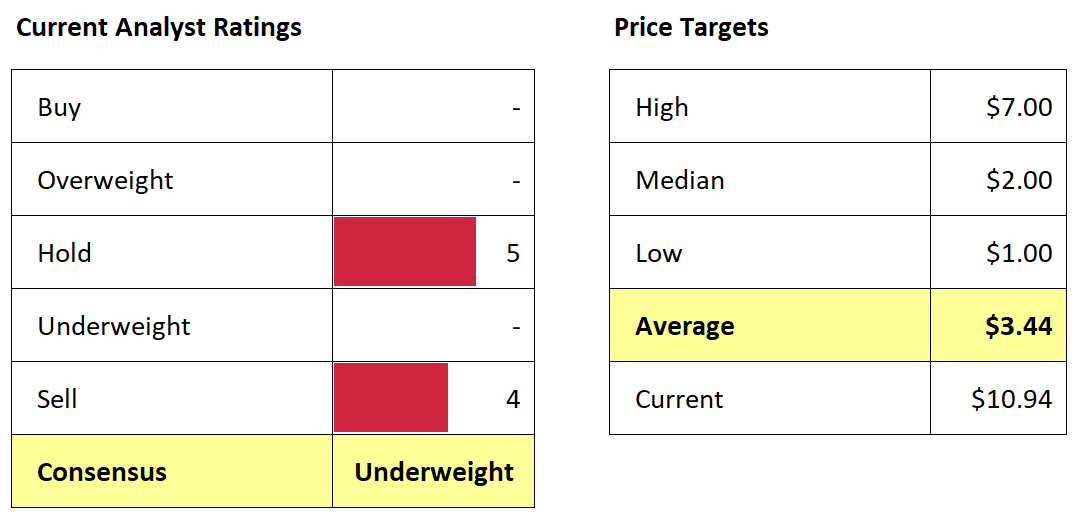

The Street’s Opinion

Surprisingly (to us at least), five out of nine analysts have “Hold” ratings for AMC, taking the “wait-and-see” approach. That said, the remaining four have “Sell” ratings.

However, these analysts’ price targets are all well below current trading levels.

Data as of 3/25/2021

Recent News

AMC Theatres® to Have 98% of Its U.S. Locations Open Beginning Friday, March 19

AMC Burbank 16 and AMC Century City 15 to Reopen Monday, March 15

Curtains Down?

The pandemic crippled businesses across the globe, but the entertainment industry endured a particularly heavy blow. When times are tough, people tend to cut discretionary expenses first — movies might be a cultural staple, but they aren’t a budgetary staple.

AMC’s financial troubles nearly caused the massive theatre chain to collapse. However, the collective power of social media retail investors clutched AMC from the verge of bankruptcy and granted the company enough time to at least try to climb out of its financial hole. Investor demand propped up the company’s stock price, enabling AMC to issue almost a billion dollars worth of shares.

Unfortunately, it looks like a bandaid on a bullet wound.

AMC’s short-term fix staved off imminent bankruptcy, but liquidity issues still loom large. Beyond the hope that movie-goers return to theatres in hordes (assuming film companies release them theatrically), the company must conquer a mountain of deferred rent and long-term debt. The numbers just aren’t working in AMC’s favor. Everything has to go right for AMC over the next 12 months — and, even then, that might not be enough.

GameStop and AMC have similarities. They’re both leaders in their spaces. They both cater to consumers and fall within the “discretionary” category. They both became social media sensations. But GameStop appears better positioned to rebound from its pandemic woes. While their business model makeover still involves risk, GameStop is pivoting for growth; conversely, it feels as if AMC is just trying to stay alive at this point.

Although we coincidentally own a single share of AMC, we do not recommend AMC at this time.

Keep an eye on (1) the 2021 film slate and what channels they release through; (2) news about theatre attendance levels; (3) July’s deadline for A-list subscribers to renew their membership; (4) AMC’s rent and debt negotiations; and (5) potential new share issuances, which would further dilute the stock’s value.

Sources

Want our free stock coverage in your inbox? Sign up now so you don’t miss our reports.