The Big Picture

It’s a good time to be a cryptocurrency investor, which might qualify for understatement of the century. Led by Bitcoin’s rally past the $60,000 milestone, the crypto market has soured in 2021. This momentum couldn’t have come at a better time for Coinbase Global, Inc. (COIN), which became the first major cryptocurrency exchange to go public when it listed on the Nasdaq last week (April 14).

Coinbase chose to go public via a direct listing, so it didn’t undergo the traditional underwriting process that helps evaluate and price a stock. As a result, Nasdaq offered a “reference price” of $250 per share, which was based on recent private market trades and the input of investment firms. However, the expectation was that COIN would open at an even higher price — and it did.

Within minutes of listing, COIN surged to almost $430.

Roughly a week later, it’s tumbled below $300.

So, is it time to cash in or cash out?

Here’s our two cents.

The inner workings of “crypto” and related technology can be a doozy to explain. So, if you’re unfamiliar with these concepts, here are Coinbase’s educational materials that you can peruse to better your understanding:

The Business

Brian Armstrong, a former Airbnb engineer, founded Coinbase in 2012. The company’s premise was simple: anyone, anywhere should be able to send and receive Bitcoin in an easy and secure fashion.

Why they would show Bitcoin’s price plummeting in their company-designed product image is beyond me.

Almost a decade later, Coinbase looks radically different. Now, it’s a leading provider of end-to-end financial infrastructure and technology for the cryptoeconomy — a financial system for the internet age that leverages digital assets built using blockchain technology.

Coinbase is one of the most popular cryptocurrency exchanges among retail investors and institutions. By daily trading volume, it’s the largest in the U.S. and third-largest in the world. As an exchange, Coinbase enables users to convert currencies and buy and sell crypto assets. However, the company’s goal is to be much more than that; Coinbase wants to provide a full service, diversified platform to the broader cyptoeconomy.

Coinbase serves a variety of customers, including retail users (like you and me), institutions (hedge funds, money managers, and corporations), and ecosystem partners (developers, merchants, and crypto asset issuers). Originally, the Coinbase platform only allowed customers to buy and sell Bitcoin, which generates transaction fees. Now, it supports over 90 crypto assets — and offers several subscription products, including Store, Save, Stake, and Borrow & Lend (aptly named, if you ask us).

Exhibit A: Product History

These additional products and services generate revenue based on a percentage of assets, reducing Coinbases’s dependence on trading volume (and transaction fees), which is highly volatile. Going forward, Coinbase also plans to monetize products (Distribute, Build, and Pay) for its ecosystem partners based on fixed fees and/or usage.

Coinbase has big plans to expand its revenue sources, but, as of right now, about 96% of the company’s total revenue is derived from transaction fees and crypto asset sales.

Here are descriptions of Coinbase’s revenue sources:

Transaction fees (retail and institutional): As an exchange, Coinbase provides matching services when customers buy, sell, or convert crypto assets on its platform. This generates transaction fees. Practically all of Coinbase’s transaction fees come from retail customers (roughly 95% in FY20) compared to institutional customers.

Crypto asset sales: Coinbase’s realized gains from sales of its own cryptocurrency holdings.

Custodial fees: Coinbase provides offline storage accounts to customers, which generate monthly fees based on a percentage of assets under custody. Customers can terminate these accounts at any time.

Staking: If you aren’t familiar with blockchain, this concept can be a little complicated. In short, the company helps create and validate blocks on various networks. In exchange, Coinbase receives the native tokens of these networks (e.g. Bitcoin, Ethereum, etc.).

Earn campaign: Coinbase’s platform enables crypto asset issuers to engage with and teach users about new cryptos through educational tools, videos, and tutorials. In exchange for completing a task (e.g. watching a video, downloading an app), users can receive cryptos from the issuer. Since Coinbase enables this transaction, it earns a commission from the issuer based on the amount of distributed cryptos. These commissions represent Coinbase’s Earn campaign revenue.

Interest income: Coinbase holds customer custodial funds and cash at certain third-party banks, which earn interest. Note: for most companies, interest income isn’t presented as revenue. Since Coinbase acts as an agent for cryptocurrency conversions and transactions, it’s not surprising that interest income rolls into revenue.

Other subscriptions: Revenue earned from early-stage services, such as subscription licenses.

Key business metrics

Coinbase tracks and reports several metrics:

Verified Users. This includes retail users, institutions, developers, merchants, and asset issuers.

Monthly Transacting Users (MTUs). Coinbase defines this as a retail user who actively or passively transacts in one or more products at least once during a rolling 28-day period

Assets on Platform. This is the total dollar value of both fiat currency and crypto assets held within the Coinbase ecosystem.

Trading Volume. This is the total dollar value of executed trades.

These aren’t official, GAAP-compliant metrics, but the company uses them to measure performance, identify trends, formulate projections, and make strategic decisions.

Verified Users

According to the company’s latest earnings call, its Verified Users were 56 million as of March 31. So, Coinbase has more than doubled its user base since the beginning of 2018.

Exhibit B: Verified User Growth (2018 - 2020)

Monthly Transacting Users

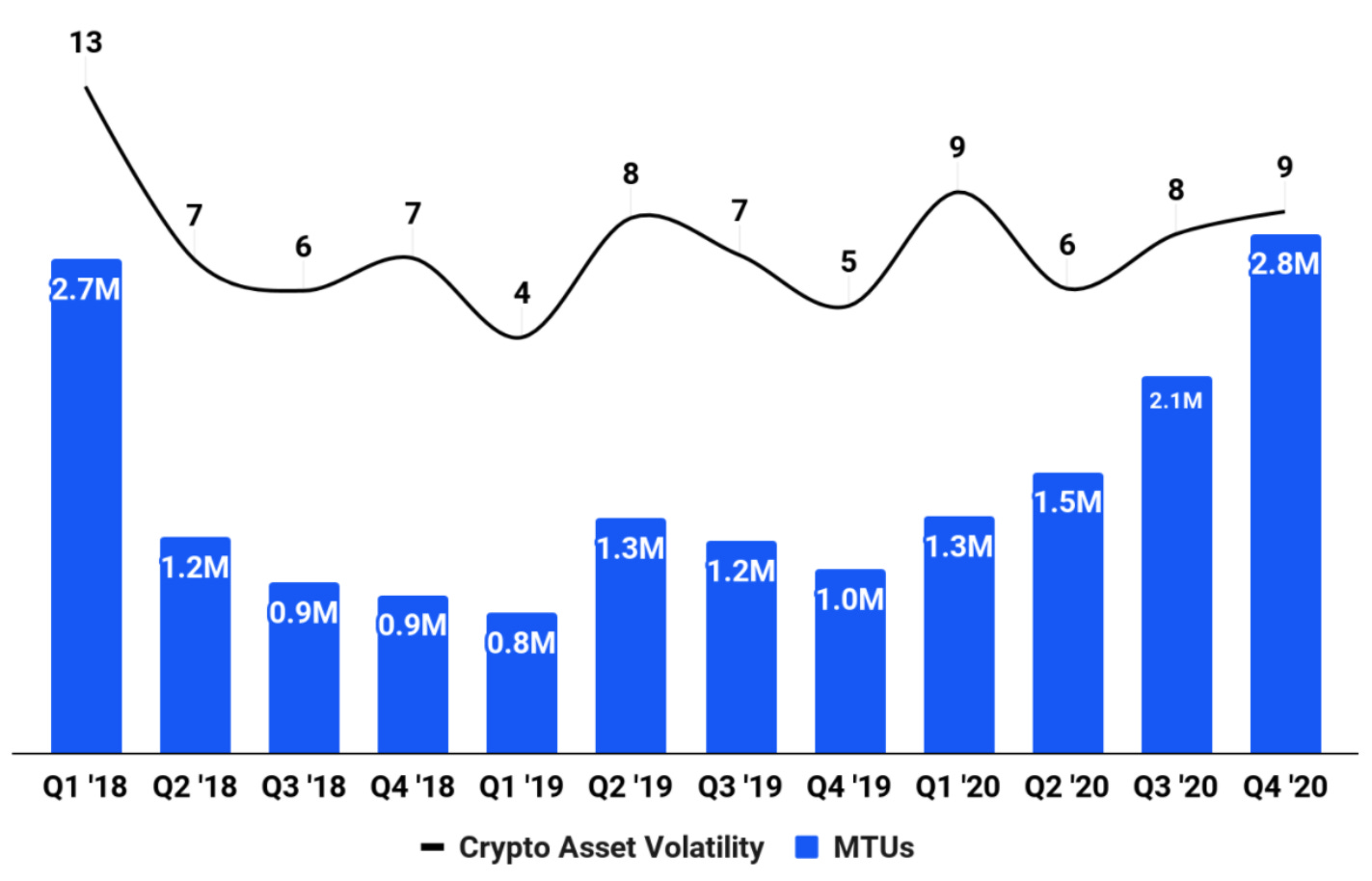

In late 2018, Coinbase started releasing subscription products and services, which increased engagement across the platform. Although the company doesn’t share pre-2018 data, it states that MTUs seem to be less correlated to broader crypto asset volatility; however, MTUs remain correlated to Bitcoin prices.

Coinbase’s MTUs exploded alongside the crypto mania of early 2021. As of March 31, the company had 6.1 million MTUs — a significant increase from prior periods.

Exhibit C: Monthly Transacting Users (2018 - 2020)

Assets on Platform

Price, quantity, and type of asset drive the Assets on Platform metric, so it tends to fluctuate. For example, when Bitcoin and Ethereum plummeted in 2018, Assets on Platform decreased significantly too. That year, Bitcoin and Ethereum prices fell approximately 74% and 82%, respectively, and the total crypto asset market capitalization decreased by 80%.

Coinbase’s Assets on Platform decreased by 73% during the same period. However, the crypto market has obviously rebounded since then — and this metric has drastically improved in that time. As of March 31, the company’s Assets on Platform was $223 billion.

Exhibit D: Assets on Platform Growth (2018 - 2020)

Trading Volume

When the company experiences high levels of trading volume, transaction revenue spikes. Business is good. When trading volume dips, so too does transaction revenue.

And both Trading Volume and transaction revenue are influenced by Bitcoin’s price and broader crypto asset volatility. So, Coinbase rises and falls with the crypto market.

The biggest takeaway from the below chart is the significant increase of Institutional Trading Volume in 2020. Companies like Tesla and Square made massive investments in Bitcoin, resulting in upward price pressures across the crypto market.

In the first quarter of 2021, Coinbase’s Trading Volume rapidly escalated to $335 billion. It’ll be interesting to see the volume split between retail users and institutions when results are officially reported.

Exhibit E: Trading Volume (2018 - 2020)

Growth strategy

Coinbase grows as the cryptoeconomy grows. It’s not a secret, that’s actually the company’s opening line within their growth strategy overview.

Beyond banking on an increasingly infectious fervor for cryptocurrency, Coinbase’s growth strategy includes three core objectives:

Adding more customers

Expanding the depth and breadth of assets

Launching innovative products

Adding (and engaging) more customers

At the conclusion of 1Q21, Coinbase had 56 million Verified Users; however, it only had 6.1 million active users (based on MTUs). Despite its recent successes, this actually represents an area of improvement. To increase adoption and engagement, the company has several objectives, which we’ve condensed into the following key points of emphasis and stats:

Increase outbound marketing. Last year, Coinbase spent less than 5% of net revenue on sales and marketing. Since inception, over 90% of its retail users found the company organically or through word-of-mouth. Going forward, Coinbase plans to expand marketing efforts across new and existing media channels.

Enhance institutional coverage and support. The company notes that verified institutional users grew from 4,200 to 7,000 firms in FY20 (a 67% increase). In addition, Assets on Platform from institutions grew 590% from $6.5 billion to $44.8 billion in the same year. But there’s still a lot of room for growth. As mentioned above, 95% of transaction fees in FY20 came from retail users (versus institutions).

Build stronger relationships with the developer community by holding and/or participating in developer conferences for builders in the cryptoeconomy.

Improve access via additional payment methods. A historical example: the company enabled customers to link and use their PayPal accounts 2019.

Expand internationally into more markets. Much to my surprise, practically all of Coinbase’s revenue comes from the United States (76%) and Europe (24%). The company has customers in over 100 countries, but based on that statistic, customers outside of the U.S. and Europe account for less than 1% of Coinbase’s revenue. In other words, they’re so small they get buried by decimal rounding.

Supporting and investing in more assets

This one is pretty straightforward: Coinbase plans to continue adding crypto assets to its platform. Beyond that, Coinbase also wants to support new features of blockchain protocols (like staking and on-chain governance). This helps the company offer a broader suite of financial services unique to the cryptoeconomy.

Launching innovative products

The company has broad (and ambitious) plans to launch innovative products based on retail/institutional users’ and developers’ needs. Here’s a summary:

Become the go-to for everything crypto. For example, last year, the company enabled institutional customers to instantly invest in crypto assets without pre-funding their trade by launching support for post-trade credit. On the retail side, Coinbase added support for staking, which lets users earn rewards on their crypto asset holdings.

Increase partnerships. For example, in 2019, the company partnered with Visa and launched the Coinbase Card. This is a debit card for customers in select European countries that enables crypto assets to be spent at merchants who accept Visa.

Be at the forefront of infrastructure technology. Coinbase plans to invest in technology to (1) broaden education/rewards by increasing connections between crypto asset issuers and retail users; (2) provide authentication and authorization services to ecosystem partners, which streamlines login processes for customers; (3) provide developer toolkits to make it easier to build crypto-based applications; and (4) provide external-facing application programming interfaces (known as APIs) to helps developers integrate buying and selling functionality into their applications.

Lastly, Coinbase supports the broader cryptoeconomy by investing in related companies and technologies via Coinbase Ventures, the company’s venture capital arm. At the end of FY20, the company had invested in over 100 companies, including BlockFi, Compound, and Dharma. Based on carrying amount, the company’s strategic investments were collectively valued at $26.1 million at the end of FY20.

The Narrative

It’s been a banner year for cryptocurrency, which means it’s been a banner year for Coinbase. You’ve probably put this together by now, but Coinbase’s performance is directly correlated to the growth of crypto. As of today, that’s not a bad thing.

We mentioned these results individually above, but here are Coinbase’s key metrics as of March:

Verified Users: 56 million

Monthly Transacting Users (MTUs): 6.1 million

Assets on Platform: $223 billion, of which $122 billion are from institutions

Trading Volume: $335 billion

And the associated earnings estimates:

Total Revenue: $1.8 billion

Adjusted EBITDA: approximately $1.1 billion

Net Income: approximately $730 million to $800 million

Coinbase earned more in the first quarter of 2021 than all of 2020. This news broke April 6, eight days before the company’s IPO. Needless to say, Coinbase couldn’t have timed going public any better.

IPO

As we mentioned, Coinbase elected to take a less traditional IPO route via a direct listing. Here are the biggest takeaways:

Direct listings don’t involve new shares, so the company doesn’t raise capital (at least, not directly). Instead, company insiders cash out; for example, Brian Armstrong made a cool $291 million from selling a portion of his shares.

Since there wasn’t a share issuance, shareholder value wasn’t diluted.

Coinbase’s decision to forego an equity raise indicates that company management doesn’t think it needs to raise capital. That shows confidence in its balance sheet and future cash flow.

Insiders (like Brian Armstrong) don’t have a lock-up period, which could cause COIN’s stock price to rapidly fluctuate if he/other insiders sell huge batches of shares at once (which, as we mentioned, Brian already has — and could do so again).

From the company’s perspective, a direct listing offered a few benefits. First, it’s faster — which is ideal when investor demand is off the charts. More and more people want to get their hands on anything crypto. A well-known and highly successful crypto exchange had investors foaming at the mouth. Second, it’s cheaper since the company avoids deal fees (i.e. paying an investment bank to underwrite and bring the company to market). Third, as we mentioned already, it doesn’t dilute shareholder value.

Coinbase could’ve raised hundreds of millions of dollars, but it decided not to. So, that begs the question, does Coinbase really not need the capital?

Capital resources

No, it doesn’t. At least, not at the moment. And we can base this sentiment on two facts:

At the end of FY20, Coinbase had $1.06 billion of unrestricted cash and cash equivalents.

At the end of FY20, Coinbase didn’t have any “traditional” debt; the company did have unsecured Crypto asset borrowings of $271 million.

So, the company’s cash position is almost four times greater than its outstanding crypto debt. That doesn’t even include $187.9 million of crypto assets and another $48.9 million of USDC, a stablecoin that can be redeemed at a one-for-one rate for U.S. dollars.

Considering the recent trend, we wouldn’t be surprised to see Coinbase issue convertible notes at zero or negligible interest rates.

Long story short, Coinbase has a healthy balance sheet — but the bigger question is if Coinbase can insulate itself from crypto’s volatility. The company can exert some control over that by broadening and emphasizing its subscription-based products. However, the company is also at the mercy of the crypto market.

The good news is that crypto is becoming more legitimate in the eyes of major businesses.

Legitimacy

There was a time when most people scoffed at or heavily doubted the legitimacy and relevancy of cryptocurrencies — back when Bitcoin traded for a few bucks and blockchain sounded like a cumbersome necklace. I did, you did, everyone did.

That’s not the case anymore. Now, even institutional investors recognize this market and regularly trade cryptocurrencies. Based on data collected from Fidelity Digital Assets and Greenwich Associates, Insider Intelligence compiled the following table:

Out of 393 U.S. institutional investors surveyed, 27% were exposed to cryptocurrencies in 2020. That percentage is expected to climb to 40% by the end of this year. Institutions command much larger pools of funds than the typical retail investor, so these types of customers can generate a lot of profits for crypto companies like Coinbase.

The Competitors

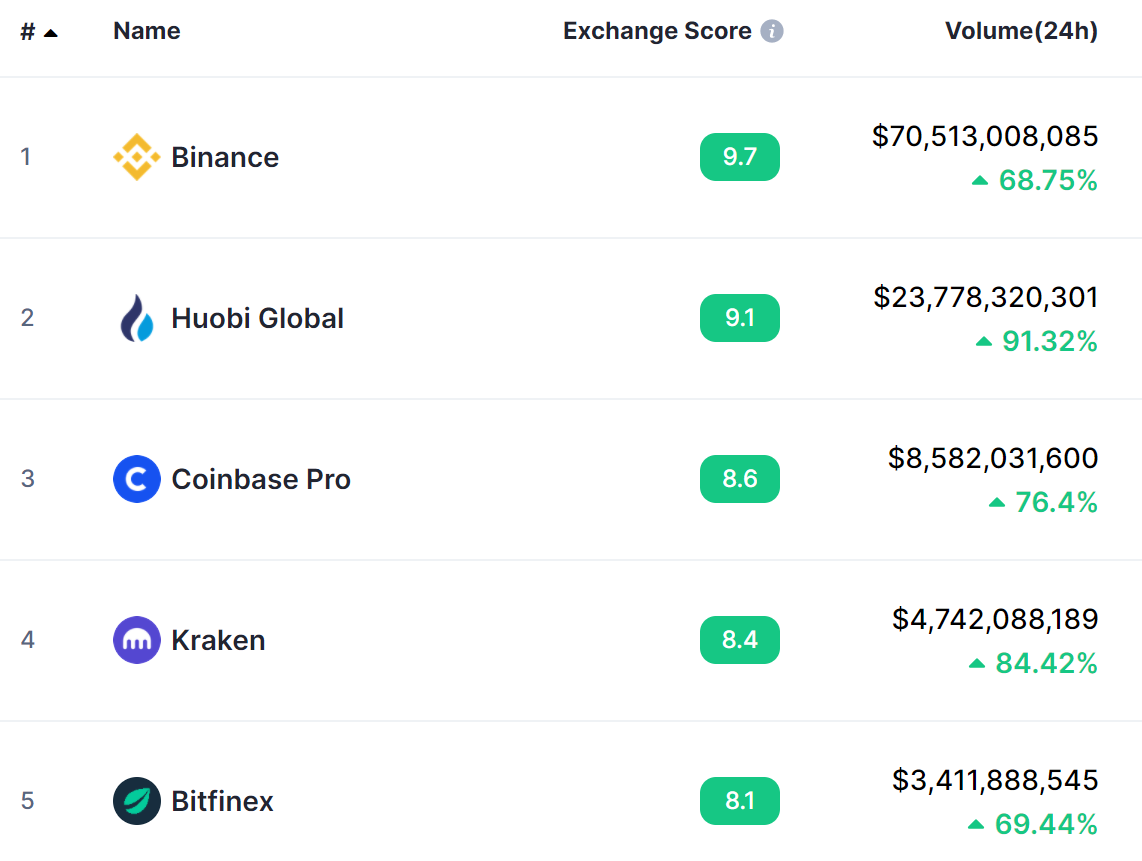

As the first major cryptocurrency exchange to go public, Coinbase’s primary competitors are private companies. According to CoinMarketCap, Coinbase is the third-largest exchange by volume, behind Binance and Huobi Global.

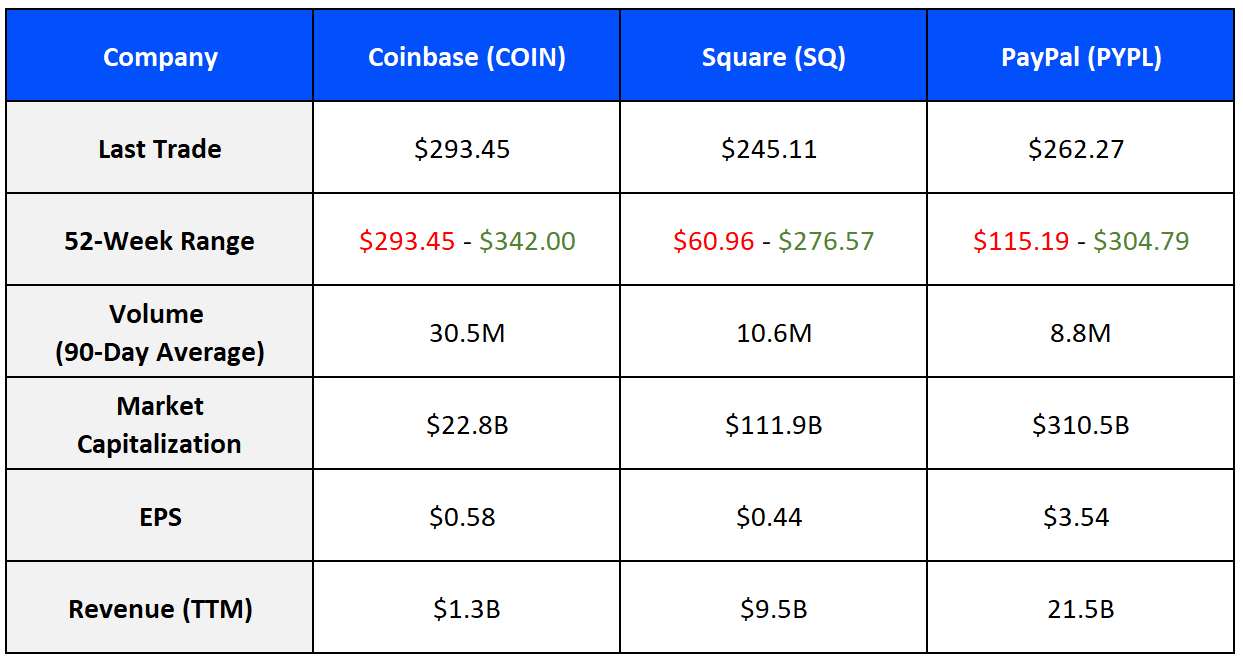

As digital payment processors, Coinbase is somewhat comparable with PayPal and Square. Note that data is as of 4/22/21.

Clearly, investing in the money business isn’t cheap. Biggest takeaways:

Investor demand is feverish. How else do you explain three times as much trading value as SQ?

Coinbase’s market cap is a fraction of these two payment behemoths.

Coinbase’s EPS will get a major boost after 1Q21 results are officially released.

Coinbase’s trading price exceeds both companies, yet, it generates much lower revenue. Again, that’ll look different after the next earnings release — but it’s still a significant drop off that potentially suggests an overpriced stock.

The High-Level Finances

Since COIN only recently went public, we don’t have access to financial results before FY19. *Coinbase’s first quarter results are not official; they’re approximations provided by company management during their latest earnings call.

Note that all dollar amounts are illustrated in millions.

Revenue

For only nine quarters of results, there’s a lot to unpack here. First, I want to share a bit of insight provided within the COIN prospectus: from inception (2012) through the end of 2020, Coinbase generated $3.4 billion of revenue. So, if we back out FY19 and FY20 revenue (collectively, $1.8 billion), that means the company generated $1.6 billion from FY12 through FY18.

Hold onto your socks: in the first quarter of 2021, Coinbase not only generated more revenue than it did in all of 2020 (which is already a staggering accomplishment), but it also made more than the company’s first seven years of revenue combined.

Transaction fees are the predominant driver, which are heavily tied to trading volume, but it’ll be interesting to see Coinbase’s revenue mix in Q1. The company wants to expand its revenue sources and insulate itself from the crypto market’s trading volatility.

EBITDA

EBITDA (earnings before interest, taxes, depreciation, and amortization) is a metric used to gauge a company’s operating performance. A company’s operations can appear worse due to certain non-cash expenses, such as depreciation and amortization.

We’ve illustrated Coinbases’s reported Adjusted EBITDA, which primarily accounts for (a) stock-related compensation (a non-cash expense), (b) impairments (also non-cash), and (c) restructuring costs (a relatively immaterial amount that only impacted FY19).

Coinbase experienced a drastic Adjusted EBITDA increase in FY20; going from $24 million to $527 million is not a small feat. To give you a point of reference, Square — which we covered in our last report — had an Adjusted EBITDA of $323 million in FY20. This also highlights the company’s ability to generate revenue (at least, in the form of transaction fees) without escalating expenses.

Net Income

According to the Q1 news release, net income is expected to be between $730 million and $800 million. After generating $24 million of profit last year, that’s insane growth. Again, this all boils down to rapidly escalating trading volume and the associated transaction fees. But, to the company’s credit, Coinbase also managed to achieve these heights without traditional debt — so its bottom line isn’t hurt by interest expense.

It’s impossible to say if this level of trading activity (and growth) is sustainable at this point in time. However, this further reinforces the company’s strengths of liquidity and available capital to invest in expanding its products and services.

The Primary Strengths

Ride with crypto. The cryptocurrency market is booming, which is helping Coinbase make money hand over fist. Coinbase has already surpassed last year’s revenue after only one quarter.

Market share and potential. Coinbase will forever be the first major cryptocurrency exchange to become a publicly traded company. On top of that, it’s an early innovator within the cryptoeconomy. It’s well-positioned to take advantage of crypto’s growth and the underlying technologies’ adoption.

Growing institutional interest. To date, retail investors have generated the vast majority of the company’s revenue. However, it’s clear that institutional interest in the crypto market is growing. This is an entirely different (and capital-flushed) customer base. If Coinbase can entice more institutions to its platform, that would significantly benefit the company’s earnings and revenue mix.

Capital structure. Part A: Coinbase had $1.06 billion of unrestricted cash and cash equivalents at the end of 2020. Part B: Coinbase doesn’t have any outstanding debt. Part C: Coinbase didn’t need to raise capital via an IPO, so they pursued a direct listing; in turn, it didn’t dilute shareholder value by issuing a bunch of new shares. Altogether, that’s a recipe for a healthy balance sheet.

The Primary Risks

Die with crypto. An exchange is only as good as the products it helps people buy and sell. It’s not a secret that cryptocurrencies are volatile and speculative investments — so much so that the company didn’t issue revenue guidance for FY21. If there’s another mass exodus like the 2018 cryptocurrency crash (when Bitcoin’s price dropped 65% in a month), Coinbase’s revenue — and stock price — will take a serious hit.

The rise of competitors. If Coinbase’s competitors offer similar services at reduced or even zero fees, that would be bad for business.

Concentration risk. Although Coinbase is a global company, practically all of Coinbase’s revenue comes from the U.S. and Europe. If these territories crack down on crypto or impose hefty capital taxes on crypto, that could adversely impact Coinbase’s business.

Legal complications. As Coinbase expands into additional markets, it’ll have to appease and comply with laws, rules, and regulations of a variety of jurisdictions. Failure to do so could subject the company to lawsuits and fines.

Impairment potential. Cryptos are volatile assets, and Coinbase holds a sizable portfolio of cryptos on its balance sheet (valued at $316 million at the end of 2020). Each year, the company tests the fair value of these assets; if these cryptos’ market values have declined, the company will recognize an impairment charge. Although it's a non-cash expense, this will hurt earnings — which could scare off potential investors.

The Street’s Opinion

COIN doesn’t have a ton of coverage yet, as only seven analysts issued ratings. However, six out of seven analysts are bullish; COIN received five “Buy” ratings and one “Overweight” rating compared to a single neutral “Hold” rating.

Price targets are all over the map — but it’s worth noting that the lowest prediction ($285) isn’t far below the current trading price. Note that data is as of 4/22/21.

Recent News

Coinbase Chief Executive Armstrong sold $291.8 million in shares on opening day

Coinbase Announces First Quarter 2021 Estimated Results and Full Year 2021 Outlook

Spare any change?

Although Coinbase has been around for almost a decade, its story as a publicly traded company is still in the opening chapter. The company’s prospectus only provides insight into 2019 and 2020 (and some aspects of 2018). Beyond the high-level Q1 announcement, there isn’t much other public information to analyze. However, from what we can analyze, the company’s financially healthy and capital-capable — and could secure cheap debt via convertible notes if that trend continues, which would enable Coinbase to invest even more in its product development.

An investment in Coinbase is really an investment in the broader crypto market and “cryptoeconomy,” as Coinbase likes to call it. If there’s a public company that’s positioned to benefit from crypto booms, it’s Coinbase — but the inverse is also true until the company manages to insulate itself from dips in trading volume.

If you believe in Coinbase’s long-term position as an early innovator within the cryptoeconomy, COIN could be a worthwhile investment and a way to invest in cryptocurrency without directly owning any cryptocurrency. If you’re hesitant about its attachment to cryptos and their volatility, it’s probably not the best move for you. If you’re also hesitant about its elevated stock price relative to its earnings and other comparable companies, well, that’s a reasonable hesitation too.

From a long-term standpoint, we’re optimistic and own a few shares. (For the record, we aren’t financial advisors and we aren’t persuading or dissuading you from investing in COIN.)

Keep an eye on (1) The crypto market’s price movements — particularly Bitcoin’s, as Coinbase’s trading volume and transaction fees are directly correlated; (2) Any regulatory news about crypto and Coinbase’s operations; (3) Additional exchanges and other crypto companies that could elect to go public (like BlockFi); and (4) Coinbase’s international market penetration and product/service offering expansion, which will help mitigate major risks.

Sources

Want our free stock coverage in your inbox? Sign up now so you don’t miss our reports.