The Big Picture

Cresco Labs has been around for a while, but it’s still somewhat of an under-the-radar cannabis company. That’s starting to change, as the company’s aggressive acquisition strategy has significantly scaled operations over the last year.

Nevertheless, the industry as a whole exists within a confounding legal paradox.

Thanks to our nation’s governing hierarchy that separates state and federal laws, weed is legal in some places, illegal in others, and simultaneously illegal everywhere. Fortunately, the federal government is working on resolutions.

Until then, should you be high on Cresco Labs? Or just say no?

The Business

Cresco Labs Inc. (CRLBF) cultivates, manufactures, and sells cannabis products in the United States (and operates 26 nicotine vape stores in Canada). Edit: Cresco sold its vape business, which operated under 180 Smoke. Founded in 2013, the company is headquartered in Chicago and primarily operates in 10 U.S. states: Illinois, Nevada, Ohio, Arizona, Maryland, Pennsylvania, California, New York, Massachusetts, and Michigan.

Interestingly enough, Cresco is not active (yet) in popular markets like Washington, Oregon, and Colorado. The company attributes this to loose regulatory frameworks, which create unpredictable supply-and-demand market dynamics.

Cresco employs a consumer packaged goods (“CPG”) approach. Collectively, Cresco’s portfolio consists of approximately 600 products across various brands, including Cresco, Reserve, High Supply, Good News, Wonder Wellness Co., FloraCal Farms, Remedi, and Mindy’s. Although the company owns and operates 31 retail dispensaries, it prioritizes wholesale distribution to third-party dispensaries all over the country (1,100 dispensaries as of December 2020). Cresco’s wholesale strategy helps maximize points of distribution and drive revenue growth — regardless of its own retail store growth.

Cannabis production

The cannabis supply chain consists of five stages:

Cultivation

Extraction

Testing

Distribution

Retail

The company has multiple cultivation, extraction, and processing facilities, allowing the production of cannabis products across several product categories. The company has plans to expand its cultivation space from 529,000 square feet to 1,229,000 square feet.

Recent acquisitions

Cresco has relied on inorganic growth via acquisitions to increase its market share.

In January 2020, Cresco completed its acquisition of Origin House, a California-based cannabis brands and distribution company.

In February 2020, Cresco completed its acquisition of Hope Heal Health, Inc. (“HHH”) and an affiliated real estate entity. HHH holds licenses for cultivation, product manufacturing, and retail operations from the state of Massachusetts — and can obtain two more retail licenses in the state.

In May 2020, Cresco reached an agreement to acquire Verdant Creations, which brought the company’s Ohio dispensary count to five — currently the maximum under Ohio state law. The transaction closed in February 2021.

In January 2021, Cresco announced an agreement with Bluma to acquire all of Bluma’s outstanding shares. Bluma has eight dispensaries located around Florida and seven more are in development. The transaction closed in April 2021.

In March 2021, Cresco entered an agreement to acquire Cultivate Licensing and BL Real Estate, a vertically integrated Massachusetts cannabis operator. The transaction is expected to close at the end of the year.

Growth strategy

Needless to say, the biggest driver of growth for any U.S. cannabis company is cannabis legalization across the country. As state governments continue to approve medical and recreational sales, Cresco can further scale operations. Legal cannabis sales are anticipated to reach $41 billion by 2026, so the market’s growth potential is quite appealing.

Cresco expects to continue increasing its market share in its most developed markets (Illinois, Pennsylvania, and California), while simultaneously expanding in other states such as Florida, Michigan, New York, and Massachusetts. Cresco’s growth strategy will be based on:

Pursuing acquisition of license or existing cannabis operations in other legal cannabis markets

Completing application process for new states beginning or expanding medical cannabis programs

Supporting its wholesale-first strategy with tactical build-outs of its retail footprint

Building the best portfolio of brands within the cannabis industry, supporting both today and tomorrow’s cannabis consumers

The Narrative

As I’m sure you’re surprised to hear, Cresco’s most prominent storyline has to do with the legality of its products.

Marijuana is legal in 43 states in some capacity (including D.C.) — but it remains illegal at a federal level. Cultivating, distributing, and possessing marijuana are criminal acts under the United States Controlled Substances Act (the “CSA”). The CSA comprises five tiers or “schedules”; the U.S. government recognizes Marijuana as a Schedule I drug. You know what else falls within this category? Heroin, LSD, and ecstasy.

So, cannabis companies are technically breaking the law even if they comply with state laws. Quite the conundrum, right?

Well, the U.S. government has issued guidance regarding marijuana-related business over the years, starting with the Cole Memo in 2013. The memo prioritized prevention and enforcement efforts of marijuana activities — specifically referencing criminal enterprises, gangs, and cartels. In essence, beyond large-scale criminal activity, the government would let the states handle it.

More recently, Merrick Garland, the current U.S. Attorney General, has commented that he doesn’t believe pursuing nonviolent crimes, such as marijuana possession, is a good use of federal resources.

Long story short, so long as cannabis companies (such as Cresco) comply with state laws, they should avoid federal prosecution. But that doesn’t mean the government is totally hands-off — for instance, the government launched a probe in March to investigate whether Green Thumb Industries (GTBIF) had improperly influenced the Illinois politicians involved in legalizing and licensing the sale of cannabis.

The good news for cannabis companies: most Americans support legalizing marijuana in some capacity. According to a 2019 Pew Research poll, 67% of Americans thought marijuana should be totally legal; on top of that, 91% supported the legalization of medical marijuana.

Per the National Cannabis Industry Association, here’s a geographical breakdown of marijuana legalization by state.

Banking issues

There’s a marijuana legalization subplot: since the drug isn’t federally legal, most financial institutions can’t and won’t transact with cannabis companies, such as Cresco. But there’s progress on this front too.

The Secure and Fair Enforcement Banking Act of 2021 would prohibit federal banking regulators from penalizing financial institutions for providing banking services to legitimate cannabis-related businesses. The U.S. House of Representatives passed the bill in April, so now it proceeds to the Senate.

A limited debt capital pool makes raising inexpensive debt tricky. In 2020, Cresco secured a $100 million term loan with a mutual option to increase the principal amount to $200 million, which was exercised in December. The loan carries a hefty 13% interest rate, which places a burden on Cresco’s cash flow.

This appears to be the market standard though; for instance, Green Thumb Industries’ (GTI) secured notes have a 12% interest rate. As the industry grows and further legalizes, interest rates should decline. Until that happens, earnings will take a hit at the hands of the banks willing to lend them money. Edit: GTI refinanced its debt in April with $217 million of senior notes at a 7% interest rate, so that’s a good indicator for the cannabis industry.

The Competitors

The cannabis industry is competitive — but it’s burgeoning. Over the last year, Cresco’s aggressive acquisition strategy helped its share price quadruple at one point. Cresco’s competitors have seen similar levels of share appreciation.

As you’ll see in the following table, there isn’t much variance between Cresco and its competitors in terms of market capitalization, EPS, and revenue.

The High-Level Finances

Note that all dollar amounts are illustrated in thousands.

Revenue

Cresco generates the majority of its revenue by wholesaling cannabis products to dispensaries. Wholesaling accounted for 58% of the company’s FY20 revenue, while company-owned retail dispensaries generated the remaining 42%. Retail revenue includes medical and adult-use cannabis sales in the U.S.

As you can see, Cresco’s has aggressively scaled its operations through acquisitions, leading to massive revenue bumps. The acquisitions of Origin House, Valley Ag, and HHH primarily drove last year’s growth of 217%. Increased cultivation capacity and retail expansion drove the company’s organic growth.

Adjusted EBITDA

EBITDA (earnings before interest, taxes, depreciation, and amortization) is a metric used to gauge a company’s operating performance. A company’s operations can appear worse due to certain non-cash expenses, such as depreciation and amortization. We’ve illustrated our calculation of Cresco’s Adjusted EBITDA, which also adds back share-based compensation (a non-cash expense).

Adjusted EBITDA took a noticeable hit in FY19. This was a result of increased operating expenses, which were driven by expansion into new markets and investments in the

company’s team and operational infrastructure. Needless to say, the acquisitions started paying off last year, as Adjusted EBITDA skyrocketed to $114.4 million in FY20.

Net Income

The company isn’t and hasn’t been profitable. That’s not unusual for a company that prioritizes growth. The good news is that Cresco’s operating income was positive — the loss drivers came from the bottom of its income statement (and depreciation and amortization).

In FY20, Cresco had pretty significant levels of depreciation and amortization ($40 million), interest expense ($34.7 million), and income tax expense ($43.7 million). The company entered into a $200 million loan agreement and new lease agreements for its facilities, driving the high levels of interest expense. Meanwhile, Cresco’s increasing gross profit and nondeductible expenses related to acquisitions are driving the high tax expenses.

The Primary Strengths

Growing market. Legal cannabis sales totaled $17.5 billion across the U.S in 2020. BDS Analytics projects the U.S. market for legal cannabis sales (including both medical and adult use) to reach $41 billion by 2026. It’s a growing market, which would significantly benefit from increased legalization — especially since illicit sales of cannabis are estimated to exceed $100 billion every year.

Market positioning. Although Cresco has primarily used acquisitions to scale, the company is still positioned as the largest wholesaler in the country. This strategy enables Cresco to drive revenue growth and maximize points of distribution, regardless of its retail dispensaries’ performance. So, Cresco grows alongside the cannabis market’s growth.

Capital structure. Although Cresco’s interest expense is sizable, the company still had adequate cash on hand to service debt and continue executing its acquisition strategy. As of 3/31/21, Cresco had $255.5 million of cash versus $187.9 million of debt.

The Primary Risks

Weed is illegal. I mean, this had to be pretty obvious right? As of today, the federal government still classifies marijuana as a Schedule I drug, meaning it’s an illegal substance. Legal and political proceedings aside, it feels safe to say that the federal government isn’t going to spontaneously crack down on cannabis companies that abide by state laws. That would be a huge risk from the government’s standpoint.

Technically, you could make an argument (at least, in a courtroom) that anyone who invests in cannabis stocks is aiding and abetting in illegal drug trafficking. That includes companies that conduct business with or market cannabis companies. Think about it: cannabis is a huge growth industry — federal lawsuits would eliminate a lot of jobs and spook the economy. No one wants that.

Limited U.S. debt financing options. Until legislation like the SAFE Act is passed, cannabis companies have limited access to financing. In turn, they must settle for higher interest rates and less favorable terms. Plus, this can inhibit capital-intensive growth strategies like Cresco’s. The equity markets have proven to be generous sources of capital for cannabis companies, but that doesn’t mean companies want to lean on equity issuances all the time. That would dilute shareholder value.

Deal duds. Cresco has faced acquisition setbacks in the past. In 2019, it backed away from a deal to acquire VidaCann due to financing concerns. In 2020, it terminated a deal to acquire Tryke, which Cresco management attributed to regulatory delays and the onset of the pandemic. Deals that die at the table are better than deals that turn into duds later on — but that’s still a risk when your growth strategy prioritizes acquisitions.

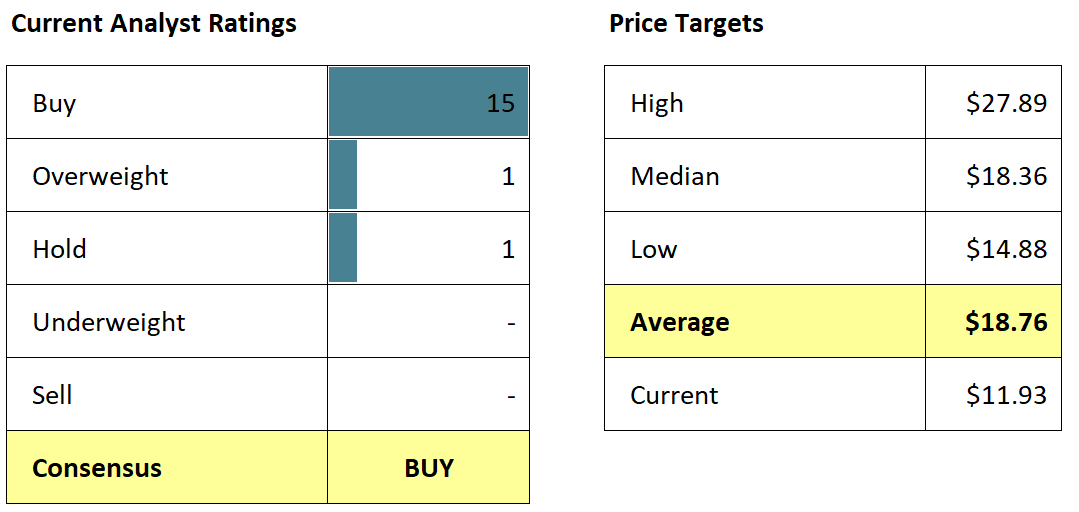

The Street’s Opinion

Wall Street’s opinion is pretty obvious: analysts like Cresco. Out of 17 total ratings, 15 analysts ranked CRLFB as a “Buy”; the remaining two were split between “Overweight” and “Hold.”

The average price target ($18.76) is well above the stock’s current price of $11.93 — even the lowest price target is almost 25% higher.

Recent News

What's Behind Cresco Labs' Better-Than-Expected Q1 Results (The Motley Fool)

Cresco Labs Announces the Appointment of Sidney Dillard to Its Board of Directors

Are we high on Cresco Labs?

It’s hard not to be high on Cresco and the broader cannabis industry. Cannabis companies face a number of legal hurdles, but we see more tailwinds than headwinds at this point.

As restrictions loosen and more illicit cannabis sales are converted to legal sales, the industry can continue growing and eventually turn out consistent profits. As of yesterday morning, the company expects an annualized revenue run-rate of more than $1 billion by the end of 2021. So, it’ll be interesting to see if Cresco achieves operational efficiencies and generates positive earnings.

Even though debt financing is expensive and harder to secure with all the regulatory obstacles, Cresco still manages to execute its growth strategy. Now Cresco is the largest cannabis wholesaler in the country — even though the company inorganically scaled its way to that title, that’s still impressive and appealing.

We like Cresco, especially at its current share price (and even Wall Street agrees with us on that point).

Keep an eye on (1) Cresco’s current and future acquisitions, which would further accelerate its scale; (2) the SAFE Act and other relevant cannabis legislation, including increased legalization in other states; and (3) any federal investigations into Cressco or its competitors.