An update on Carvana + MP Materials nears completion of Stage II

A quick fix of the latest financial happenings.

Good morning, investors!

If this is your first time with us, don’t forget to subscribe here. If you enjoy today’s issue, please hit the heart button at the end of the report.

Without further ado…

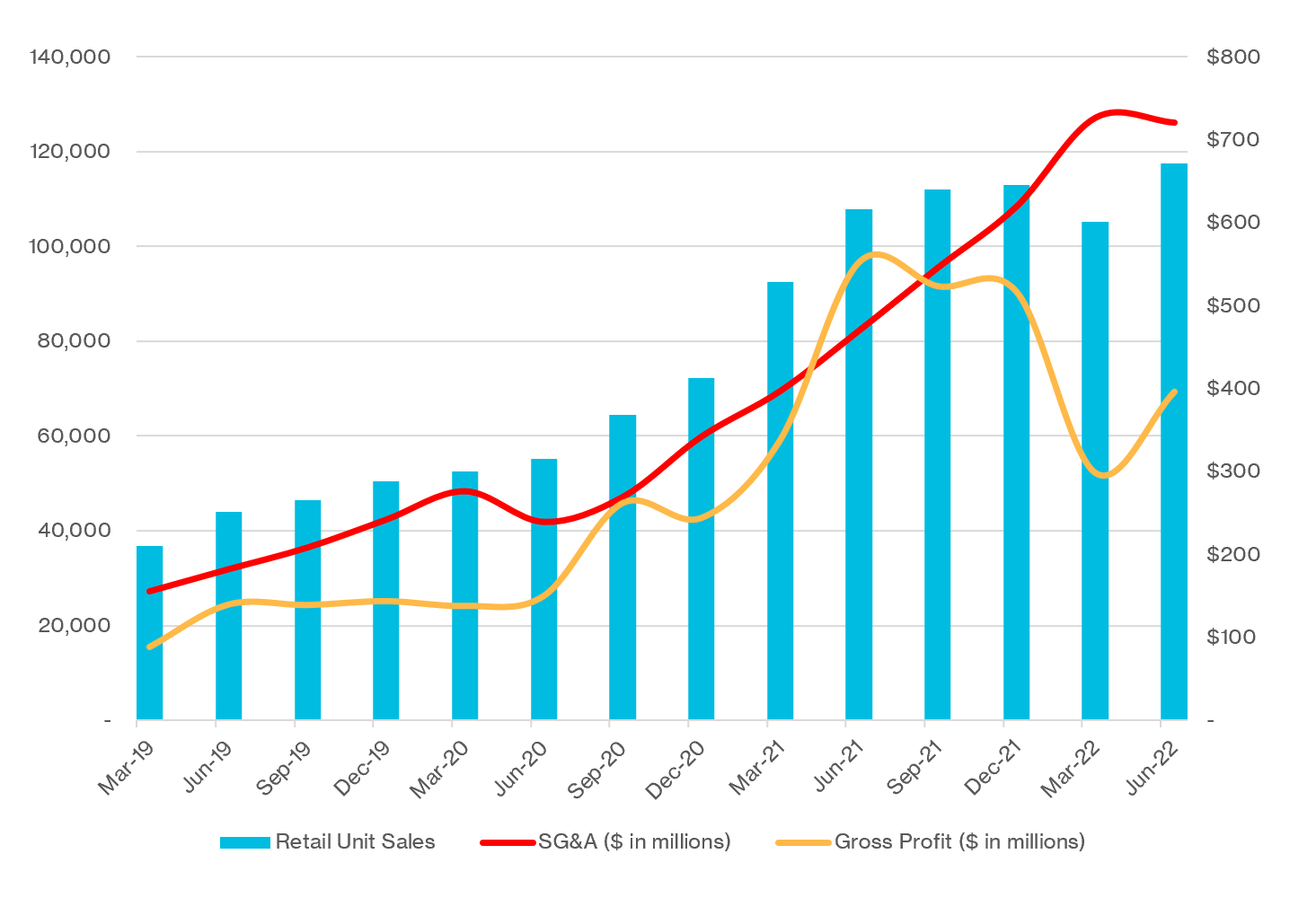

An Update on Carvana’s Aggressive Business Plan

If you recall, after profits faltered and shares endured a drubbing, Carvana announced a major business plan update in May. The company shifted its top priority from increasing retail unit sales to accelerating its path to profitability — through aggressive cost-cutting.

It was and still is an ambitious plan. To summarize, Carvana wants to maintain/continue growing unit sales while halving its overhead. The applicable metric here is SG&A per unit — essentially, overhead for every car sold.

In Q1, Carvana’s SG&A per unit was $6,912 compared to only $2,833 of gross profit per unit. Translation: Carvana lost a lot of money trying to sell its inventory.

Last week, Carvana released its Q2 results. So, how did the online car slinger fare?

Good news: Improvement! SG&A per unit fell to $6,133.

The caveat: The decline was mostly attributed to more unit sales, not less overhead. Total SG&A only fell by $6 million — from $727 million to $721 million — primarily because of less advertising expenses.

Bad news: Carvana has a long way to go to hit its Q4 stretch goal of $4,000 SG&A per retail unit sold. Aim high (or low, in this case), I suppose.

It’s not easy to increase gross profit — how much Carvana makes after buying, reconditioning, selling, and delivering its inventory — while simultaneously decreasing SG&A.

But the gap has narrowed ever so slightly.

Two Rather Positive Quotes from MP’s Earnings Call

There were plenty of positive takeaways from MP Materials’ Q2 earnings call last week. The company’s production sales and bottom line continued to benefit from high market prices for rare earth concentrate — net income increased 170% to $73.3 million compared to Q2 of 2021.

But as welcome as that is, investors are far more interested in the company’s quest to become the country’s only fully-integrated supplier of rare earth elements. (You can review my deep dive into MP Materials to better understand MP’s growth plan.)

Good news: Stage II is making great strides.

Here’s some color from Jim Litinsky, CEO and Founder of MP Materials (emboldened for emphasis):

“We remain on target for a mechanical completion by year end and we've begun pre-commissioning, which includes checkouts and initial performance testing on both legacy and new circuits in preparation for commissioning. In addition, our Stage 3 facility is going vertical and forward, and we remain heavily focused on key hires, procurement of long lead equipment and other items tracking for a late 2023 start of product for magnetic alloy.”

And there’s no shortage of demand for what MP will eventually produce. On the call, an analyst asked for more insight into potential supplier deals on the horizon given the growing electrification efforts around the country, particularly in the auto industry. Here’s Jim’s response:

“We're not demand constrained, we're supply constrained. There's a lot of interest from a lot of parties. It's not just the OEMs — it's OEMs, wind and a number of other use cases.”

Three Eye-Opening Tweets

Finally, we close with three eye-opening tweets.

A must-read thread on Disney and corporations as a whole.

Sad but true.

Investors: hungry for losses.

Thanks for reading. Don’t forget to hit the heart button if you enjoyed today’s report.

If you haven’t subscribed already, you can do so here.