Bullish Bears #2: SNAP

Is Snapchat trading at a deep discount?

Good morning, investors!

Last week, we dug into Carvana’s ambitious plan for cutting SG&A. Today, we’re exploring Snapchat’s recent tumble (plus a little overview of other beaten-down stocks).

If this is your first time with us, feel free to subscribe here. If you enjoy today’s newsletter, please hit the heart button at the end of the report.

Without further ado…

Snapchat (SNAP)

How can we not talk about Snapchat this week?

SNAP’s share price collapsed after the company warned investors that its Q2 results will likely fall short of guidance — only a month after issuing said guidance. The news hit Facebook, Twitter, and even Google share prices hard too.

Well, things haven’t been peachy since the end of April. Here’s a snippet of SNAP’s public filing that sent shockwaves throughout the market:

Since we issued guidance on April 21, 2022, the macroeconomic environment has deteriorated further and faster than anticipated. As a result, we believe it is likely that we will report revenue and adjusted EBITDA below the low end of our Q2 2022 guidance range. We remain excited about the long-term opportunity to grow our business.

Snapchat management initially expected to grow revenue by 20% to 25% year-over-year; it also expected Adjusted EBITDA to be somewhere between breakeven and $50 million.

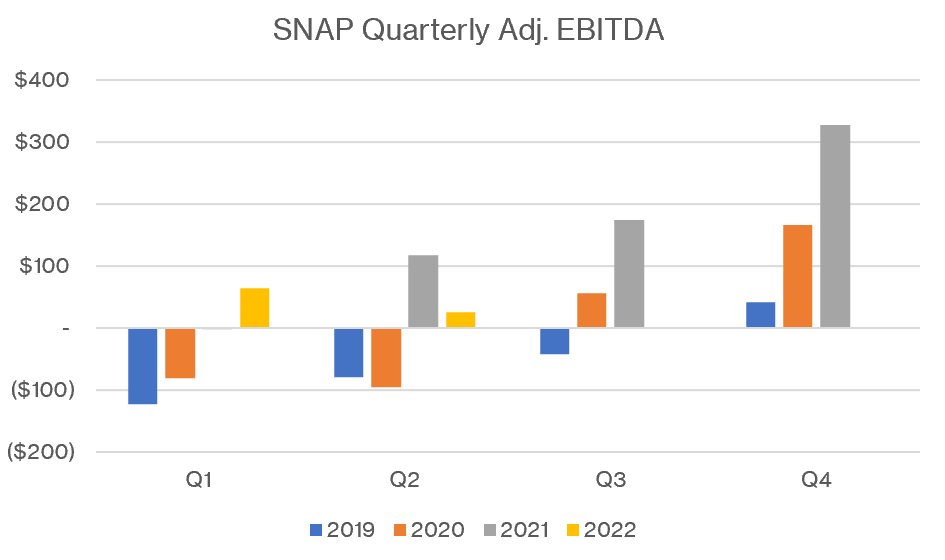

Both of these estimates would still pale in comparison to Q4 2021. To illustrate, here’s a quarterly comparison of Snapchat’s revenue and Adjusted EBITDA. Note that Q2 2022 represents the mid-point of guidance ranges.

Adjusted EBITDA, in particular, drops significantly relative to both Q2 and Q4 of last year.

Before the after-hours news, shares of SNAP closed at $22.49 per share. The next day, shares of SNAP opened at $14.50 and would eventually close at $12.80 — a 43% drop in one day. Yikes.

The concern is pretty clear: a looming recession would not bode well for a company that’s heavily reliant on advertising revenue. Investors expect SNAP operations to tank, and perhaps the consensus will be right. But let’s take a look at SNAP’s recent operating performance to see if the 43% hit is justified or a discount.

Although the photo-centric app lags behind its peers, Snapchat has steadily increased its daily active users (DAUs) over the last few years, averaging 5% quarter-over-quarter growth. While not quite as consistent, the company’s average revenue per user (ARPU) has generally trended in the right direction as well, up until Q1 of this year.

Although there’s some cyclicality, Snapchat’s operating results have improved. Revenue is up 275% since the beginning of 2019. Adjusted EBITDA has usually been positive (six of the last seven quarters). And the company finally generates positive cash flow (four out of the last five quarters).

Except you know there’s a “but” coming.

Operations have gradually moved in the right direction, but the company’s share price has outpaced its actual growth, leading to what was (and, honestly, still is) a lofty valuation.

Snapchat has traded at pretty ridiculous price-to-sales ratios during its public tenure. Its five-year average P/S ratio is 19.4. As of yesterday’s close, its current P/S ratio is only 5.3.

Even so, it’s still high.

For comparison, the five-year average P/S ratios of Facebook and Twitter — two much bigger platforms — are 9.8 and 8.8, respectively. Meanwhile, Snapchat’s P/S ratio is now more in line with those historical averages but still questionably positioned relative to its social media counterparts (FB: 4.5; TWTR: 6.2)

Could SNAP return to its former glory (i.e., $70+ per share)? Sure, but it’ll likely take a few years in the event of a recession, considering ad spend is one of the first expenses to get slashed when budgets tighten. In the near term, I expect SNAP to fall even further.

Wall Street tends to disagree. Here’s its consensus analysis:

Other Potential Bullish Bears

Here are five additional stocks that have taken a beating, as well as notable stocks from previous DD reports. I’ve provided past and present valuation metrics to give you an idea of how much investor sentiment has retreated. Note that inclusion in this table does not indicate a bullish view.

Thanks for reading. Don’t forget to hit the heart button if you enjoyed today’s report.

If you haven’t subscribed already, you can do so here.