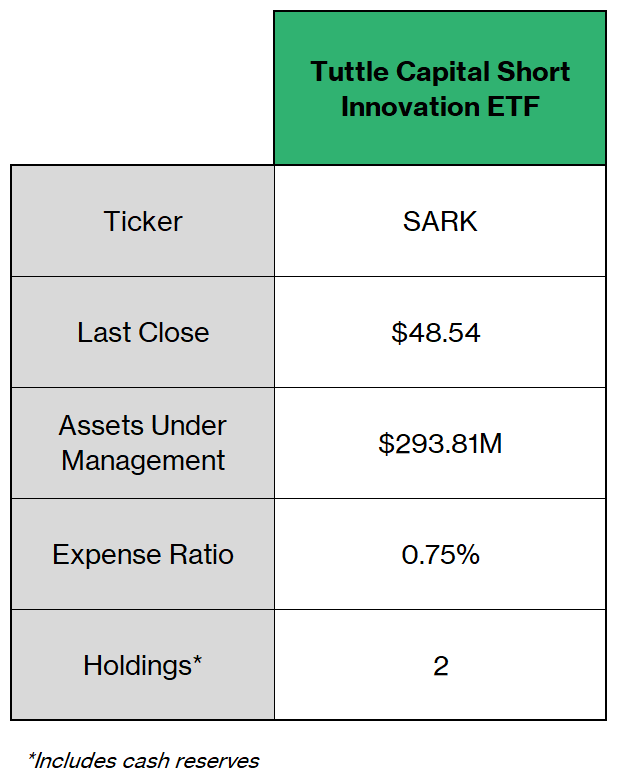

ETF Report: Tuttle Capital Short Innovation

Will SARK continue to profit off of ARKK's tumble?

Good morning, investors!

We’re back with another ETF report, except we’re flipping the script and looking at an inverse fund: Tuttle Capital Short Innovation ETF (SARK).

If this is your first time with us, feel free to subscribe here. If you enjoy today’s newsletter, please hit the heart button at the end of the report.

Without further ado…

What is SARK ETF?

The Tuttle Capital Short Innovation ETF (SARK or “the Fund”) is an inverse ETF — which is a fund that tries to replicate the opposite return of an underlying benchmark. For SARK, that benchmark is Ark Innovation ETF (ARKK). If ARKK sounds familiar, that’s because it’s the flagship fund of Cathie Wood’s capital management firm, Ark Invest (plus, I covered it in November of last year).

Long story short, if ARKK falls 2%, SARK should go up by 2%.

How does it accomplish this? By entering into swap agreements. Tuttle Capital strikes a deal with one or more financial institutions to “swap” the returns of ARKK.

This isn’t a perfect process, for a couple of reasons. First, these swaps typically last one day, so SARK usually has to place a new bet against ARKK each trading day. As a result, the Fund’s returns are unlikely to match the exact cumulative return of ARKK. More importantly, volatility — the rate of price fluctuations — amplifies the variance between these funds’ cumulative returns. (We’ll explore this more later, it’s easier to understand with numbers).

Why bet against ARKK?

Financial news outlets couldn’t get enough of Cathie Wood last year after her funds skyrocketed in both price and popularity. In 2020, ARKK generated a return of 157%.

Why bet against a fund that’s doing so well?

Because it might be doing too well.

At any given time, Ark Innovation has between 35-55 holdings — each of which falls under their thematic blanket of “disruptive innovation.” You could simplify this snazzy term to “companies of the future.” These are the stocks Ark thinks will be the driving forces behind human advancement across various walks of life, such as an internet-based business like Twilio or a financial services company that’s setting trends in its industry, such as Robinhood.

Considering the stock market is forward-looking by nature, it’s not surprising that Cathie’s funds have been so successful, especially during the pandemic’s investing boom.

But growth-oriented are not without risks; they usually operate at minimal profits (or even severe losses) and can have sizable levels of debt and scalability hurdles. And when broader market turbulence induces sell-offs, companies that are viewed as overvalued can take serious hits. (Just look at what happened after PayPal axed its growth strategy.)

Tuttle’s inverse fund makes it easy to bet against Cathie’s holdings and profit when they take a tumble.

Who runs SARK?

The man behind Tuttle Capital Management is Matthew Tuttle, who holds the titles of Chief Executive Officer and Chief Investment Officer for his firm. Here’s a quick highlight of his background:

CEO, CIO of Tuttle Capital Management (2012 – present)

CEO of Tuttle Wealth Management (2003 – 2011)

Fixed Income Sales for Bear Sterns (RIP)(1998-1999)

MBA in Finance from Boston University

Author of How Harvard & Yale Beat the Market and Financial Secrets of My Wealthy Grandparents

In September, Tuttle joined the Boardroom Alpha Podcast, Know Who Drives Return, as a guest. He shared that he was appalled by what passed as advice in the brokerage and insurance industries — so he started Tuttle Wealth Management in 2003 and staffed several advisors. As he puts it, these advisors lost his clients’ money during the housing market crisis, which pissed him off. Eventually, he launched Tuttle Wealth Management because, as the adage goes, “the only way to do it right is to do it yourself.”

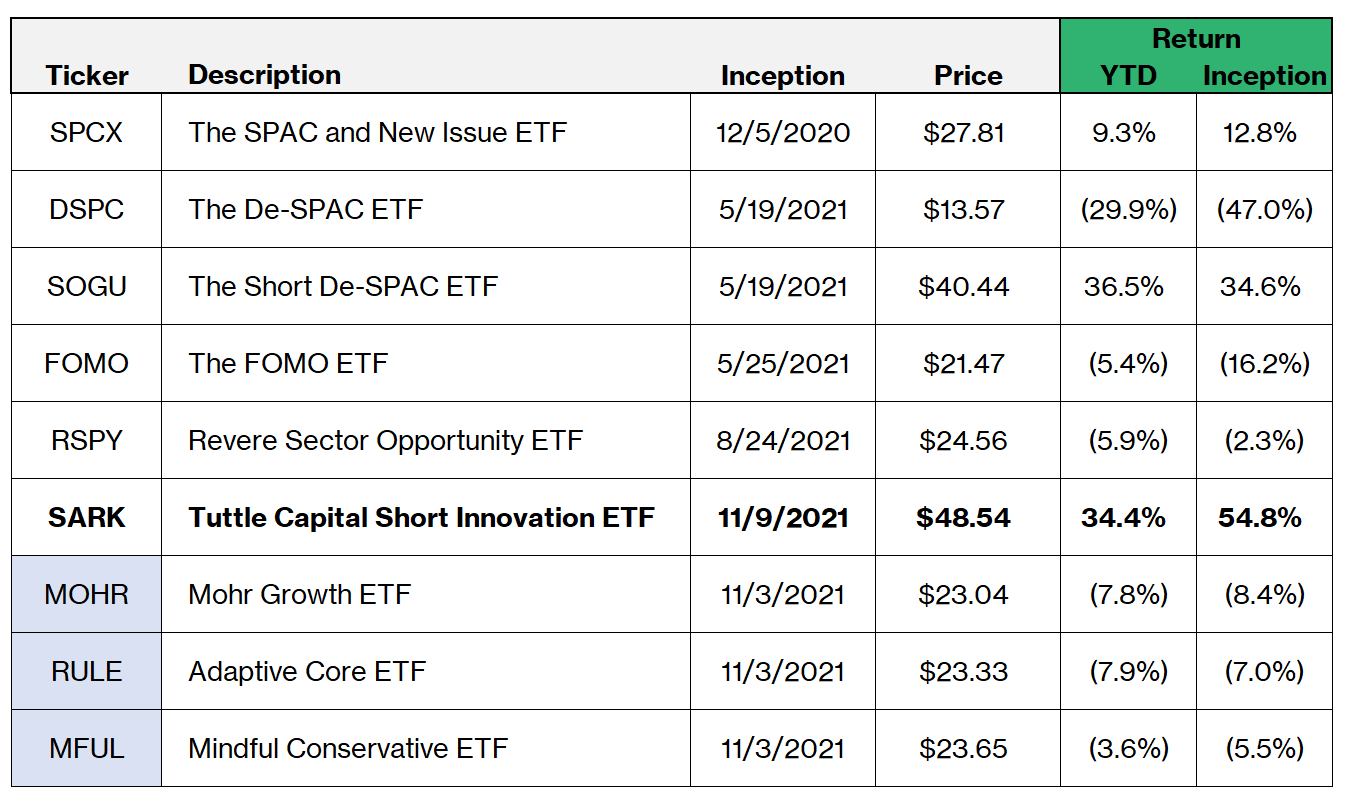

This led Tuttle and his team to start launching ETFs. Fast forward a decade, Tuttle now actively manages several thematic ETFs, which I’ve outlined below. (Note that blue-highlighted ETFs are sub-advised by Tuttle Capital.)

What does Cathie Wood think of SARK?

Like a true competitor and market participant, she welcomes the shorts.

At the Dynasty Financial Partners' 2021 Investment Forum, Wood shared her thoughts to Bloomberg:

"This is what makes a market, right? I never worry about anyone shorting the stocks underlying Ark or with this new ETF, because if we are right, they are going to have to cover their shorts and that will be another source of demand for the stocks in the future. I like skepticism, and I feel much better when there’s a good give and take."

Unfortunately for Wood, she’s been on the wrong side of that “give and take” since her comments.

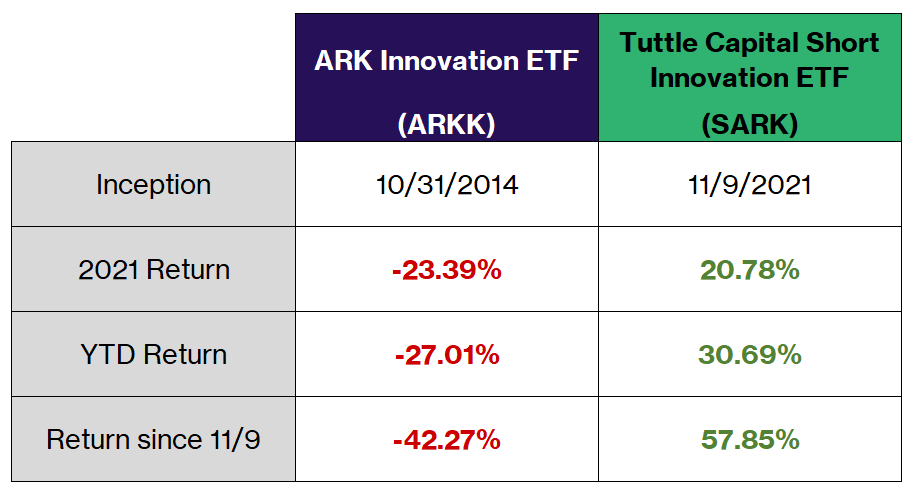

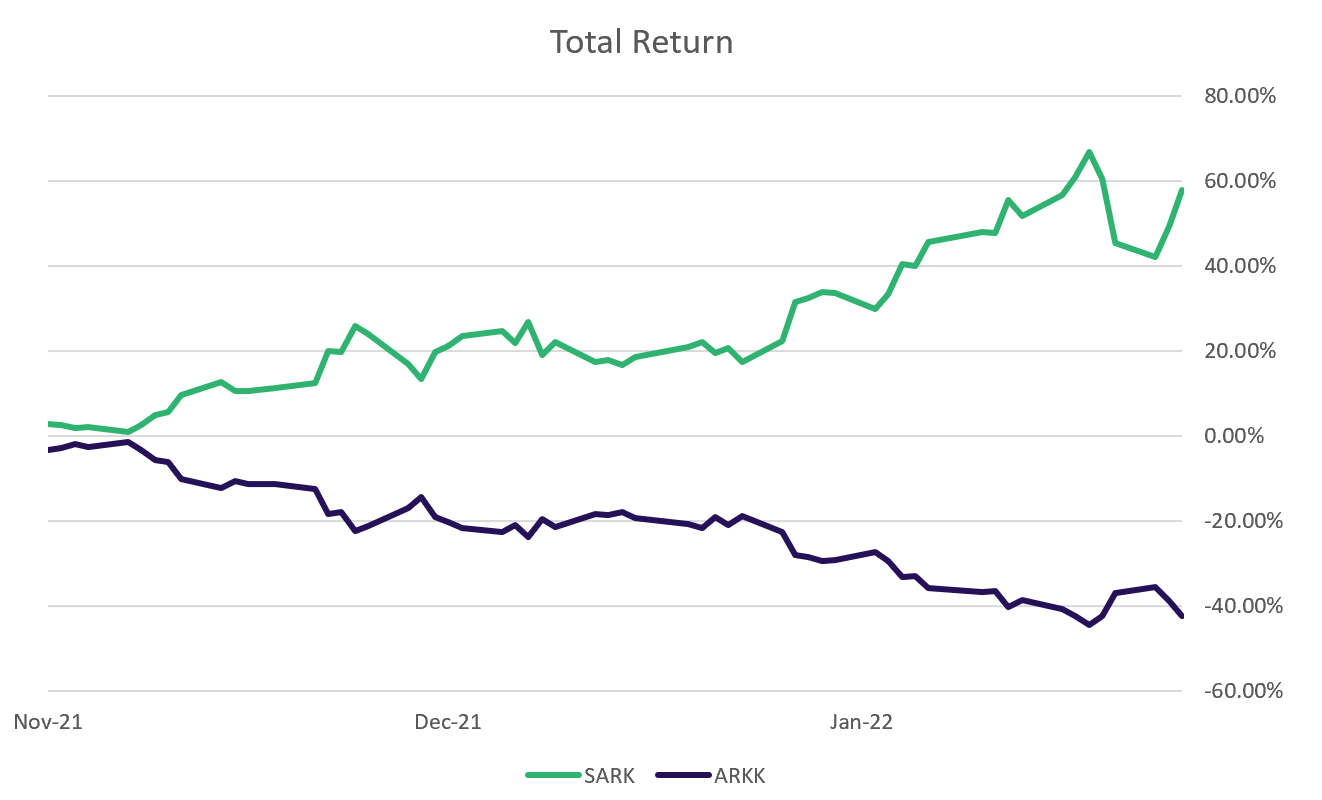

Return comparison SARK vs. ARKK

From ARKK’s inception in October 2014 through the end of 2020, Cathie and her fellow shareholders experienced stratospheric returns — 559% to be exact.

Since SARK entered the fray last November, it’s been another story.

Shorting the holdings within ARKK has proven to be quite profitable, as SARK has generated close to a 58% return in less than three months. Naturally, ARKK is in the red in that same timeframe — but we see the impact of volatility, as ARKK is “only” down 42.3%.

SARK Risks

Shorting is a gamble. It’s riskier to bet against companies than to bet on them. Buying shares of SARK is the equivalent of trying to time market downturns, which isn’t easy. It’s also *unlikely* that each of ARKK’s individual holdings will fail, especially over longer timeframes. In turn, SARK is best used as an aggressive short-term play or hedge — not a long-term investment.

SARK needs a partner. To short ARKK, Tuttle enters daily swap agreements with another institution. If that institution fails to settle what it owes Tuttle (e.g, in the event ARKK plummets one day and the firm can’t afford to pay up), it could get very messy for Tuttle and holders of its shares.

Tracking error. Since SARK is a daily bet against ARKK, the Fund is unlikely to produce an exact -100% return of ARK’s performance. This can work for or against the Fund. (Since its inception, this has worked in the Fund’s favor.)

To explain this better, here’s a hypothetical scenario from SARK’s prospectus:

Mary invests $10.00 in the hypothetical Fund after the close of trading on Day 1. During Day 2, the ARK Innovation ETF decreases from 100 to 98, a 2% loss, and Mary's investment rises 2% to $10.20. Mary continues to hold her investment through the end of Day 3, during which the ARK Innovation ETF increases from 98 to 102, a gain of 4.08%. Mary's investment declines by 4.08%, from $10.20 to $9.78.

For the two day period since Mary invested in the Fund, the ARK Innovation ETF gained 2% while Mary's investment decreased from $10 to $9.78, a 2.20% loss. The volatility of the ARK Innovation ETF affected the correlation between the ARK Innovation ETF's return for the two day period and Mary's return. In this situation, Mary lost more than -100% the return of the ARK Innovation ETF.

As the example points out, volatility is a key player — more volatility, more variance.

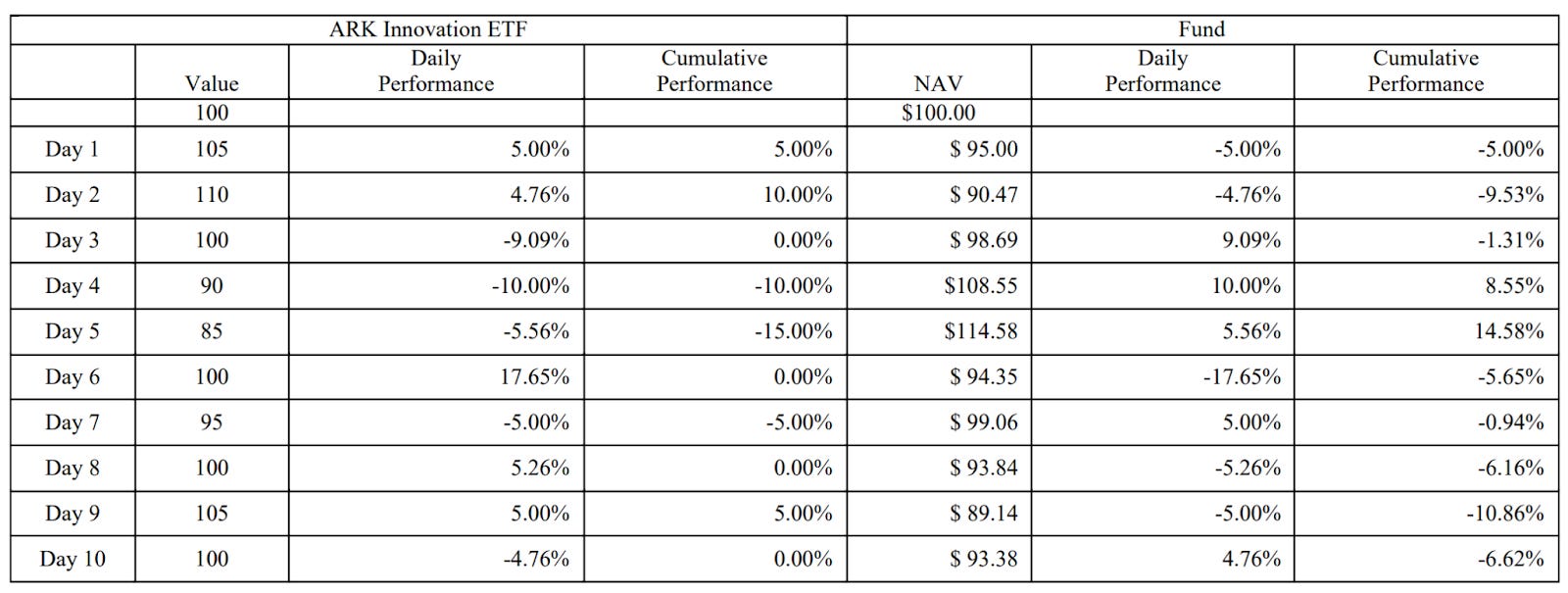

Here’s another example from the prospectus, except this time we see performance stretched out over a 10-day trading period. Although ARKK generates a cumulative 10-day return of 0%, its volatility causes the Fund to generate a -6.62% return.

SARK Outlook

Once you understand how Tuttle Capital creates an inverse return using swaps and recognize the impact (and risk) of volatility, SARK is pretty straightforward.

If you think the stocks within ARKK’s portfolio are about to struggle, SARK is a convenient way to profit from that struggle.

However, it’s certainly not a suitable investment for everyone — only investors with a near-term trading horizon who are open to aggressive short-selling strategies. That said, if you invest in ARKK and want a hedge during periods of turbulence, SARK could be beneficial too.

Thanks for reading. Don’t forget to hit the heart button if you enjoyed today’s report. If you haven’t subscribed already, you can do so here.